The municipal bond market has shown notable resilience in the third quarter of 2024, marked by an influx of supply and an increase in ownership among various investor classes, including mutual funds, exchange-traded funds (ETFs), and foreign investors, according to the latest reports from the Federal Reserve. This growth, however, comes amidst a backdrop of declining institutional ownership, especially among banks, which poses questions about the future of this significant asset class.

While it is encouraging to see an upward trend in the face amount of municipal bonds outstanding, reaching $4.171 trillion—up 2.9% from a year earlier—concerns linger regarding institutional investors whose holdings have drastically diminished. Banks have experienced a 0.3% drop from the previous quarter and a 4.3% decrease compared to Q3 2023, indicating a contraction in interest from one of the traditionally prominent players in the market.

The reasons behind the waning interest from banks in municipal bonds can be traced back to several factors, primarily weak deposit inflows and regulatory pressures that have constrained their balance sheets. A report from Wells Fargo highlights how smaller and medium-sized banks are facing deposit outflows, which has resulted in a reduced capacity to invest in municipal debt. In essence, the shrinking balance sheets of these banks hinder their demand for high-grade municipal bonds.

Despite these challenges, larger banks, which theoretically should enjoy a rebound in deposits following recent market turbulence, have not seen corresponding growth in their balance sheets. The need for regulatory reforms may be crucial, as strategists at Wells Fargo suggest that easing restrictions may pave the way for more robust demand for municipal debt, potentially revitalizing bank participation in the market.

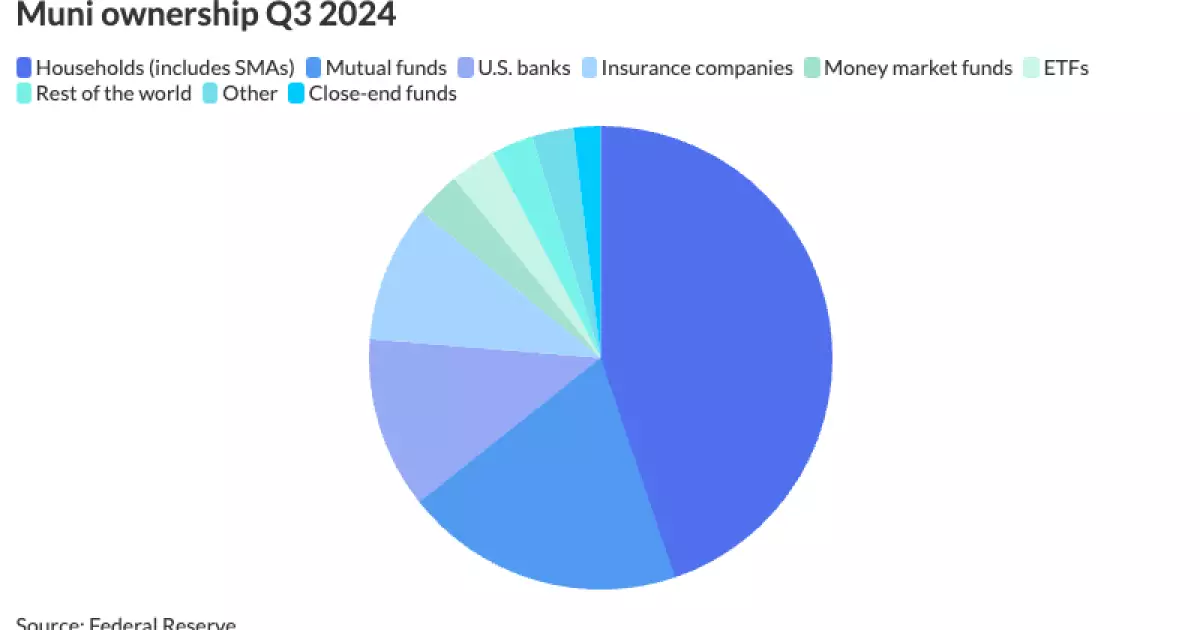

Examining the ownership composition of munis, households emerge as the largest category of owners, accounting for 44.8% of the market. Mutual funds and ETFs have also made their mark, with respective ownership stakes of 19.5% and 3.2%. Conversely, foreign investors have gradually increased their holdings, reaching $121.5 billion, marking a significant 12.3% increase year-on-year and reflecting an ongoing global interest in U.S. municipal bonds.

As household ownership climbed to $1.86 trillion—a 15.1% increase from the previous year—direct ownership through brokerage and advisory accounts has surged, mostly due to the growth of Separately Managed Accounts (SMAs). These accounts now hold a staggering sum of $1.63 trillion in munis, showcasing a shift toward individual ownership as investors seek tailored investment solutions.

The third quarter of 2024 has proven favorable for mutual funds, which rose to $810.9 billion—an 11.4% growth since the same quarter last year. However, ETFs have shown particularly robust performance, climbing to $133.3 billion, indicating a notable 23.4% increase year-on-year. This trend suggests a shift in investor preference towards the liquidity and lower transaction costs associated with ETFs, making them an attractive alternative to traditional mutual funds.

Kim Olsan, a senior fixed-income portfolio manager, noted that 2024 is characterized by a committed buying atmosphere across both ETFs and mutual funds, contrasting sharply with the asset loss seen in mutual funds the previous year. This year’s uptick in mutual fund allocations reveals a growing confidence in municipal strategies.

The Road Ahead: Regulatory Factors and Investor Behavior

The trajectory of the municipal bond market remains contingent upon regulatory developments and investor behavior. The anticipated relaxation of regulations could help to mitigate issues of capital scarcity and encourage increased participation from banks and institutional investors. Although the bond market benefits from a heightened interest in ETFs and a robust household presence, analysts remain cautious about future growth, particularly given the absence of tax-loss harvesting opportunities influencing investor strategy.

Wells Fargo strategists have indicated that while the passive investment environment is favorable, the rapid growth experienced in 2022 and 2023 may not be replicated in the near future. The dynamics are shifting, and potential competition from equities could also impact the attractiveness of municipal bonds in the broader investment landscape.

While the municipal bond market overall is experiencing significant activity and interest, concerns regarding declining bank participation, regulatory challenges, and changing investor preferences will undoubtedly shape its future trajectory. The next few quarters will be pivotal in determining how these factors will interplay and influence the direction of this vital financial space.

Leave a Reply