In the complex tapestry of the finance world, municipal bonds often represent a stable investment terrain. Recently, the municipal bond market demonstrated a surprising steadiness even as U.S. Treasuries displayed slight weakness and equities fluctuated without a clear direction. A closer examination reveals a narrative of resilience and gradual return, diverging sharply from the challenges faced in the previous year’s market.

Current Market Trends and Ratios

Municipal bonds retained their ground on Monday, showing consistent performance amidst an environment where the U.S. Treasury market felt the tremors of declining investor sentiment. Market analysts reported various ratios that highlight the relationship between munis and Treasuries, with the two-year ratio at a solid 62% and the 30-year ratio climbing to 87%, according to Refinitiv Municipal Market Data. This bolstering of municipal status reflects the ongoing interest from investors seeking security in fluctuating markets.

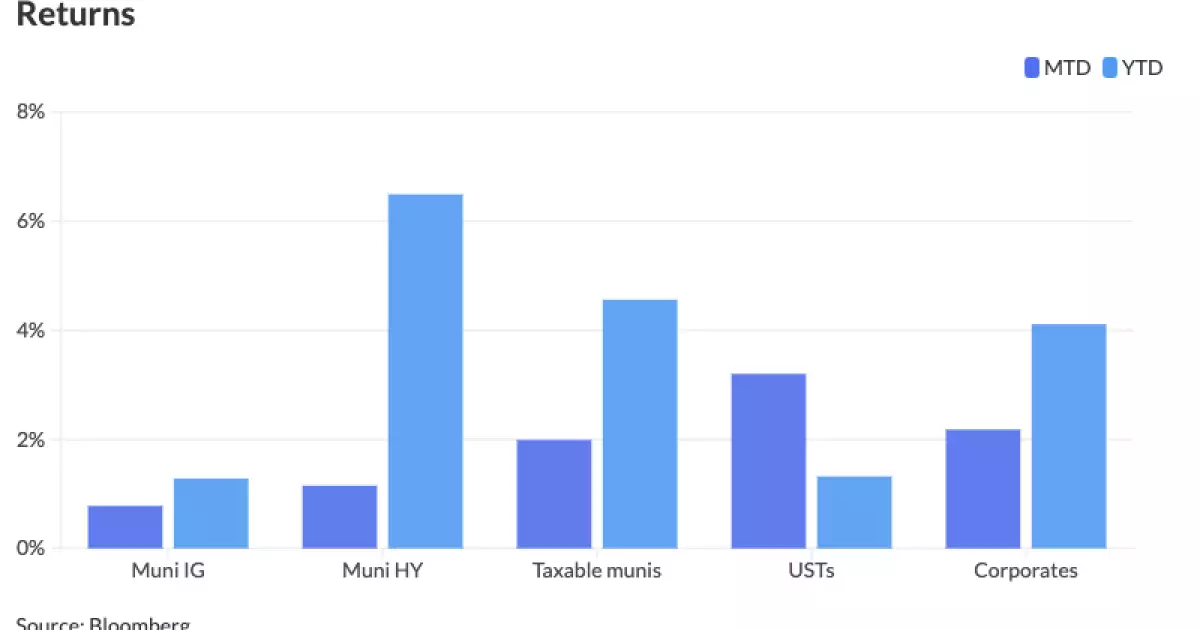

As we approach the end of August, it is worth noting this month’s municipal gains are at a notable 0.78%, although the year-to-date returns clock in at just 1.28%. Unlike the scenario in August the year prior, where losses were felt sharply at 1.79%, this year’s development portrays a recoverable optimism. Jason Wong, a vice president of municipals at AmeriVet Securities, referenced this transformation, attributing some of the positivity to Federal Reserve Chair Jerome Powell’s recent comments about prospective policy adjustments. This revelation has, according to Wong, spurred expectations for falling muni yields in response to easing Treasury yields and rising equities.

Yields and Market Reactivity

August 2023 revealed a more nuanced view of yields as they shifted broadly. Municipal yields increased by an average of 26 basis points across varied terms, with specific attention to the notable 36 basis points rise in the 10-year category. Despite these increases, recent downward trends in yields have also been noted: 10-year munis fell by an average of 2.5 basis points month-to-date. This ebb and flow suggest a market in a state of cautious optimism, driven largely by investor sentiment and Fed policy speculations.

Chris Brigati, a senior vice president at SWBC, observed that external factors, such as summer holidays, influenced market activity, contributing to a slower trading pace. Brigati highlighted that even in this less reactive environment, the secondary market began to exhibit signs of life, pushing the long-end 30-year ratios closer to significant thresholds. Investors appeared more engaged, reflected in the modest uptick in trading volumes.

Moving forward, issuance in the primary market seems stable, projected at a relatively average $8.9 billion this week. The annals of new issuances, including noteworthy deals like the California general obligation bonds by BofA Securities, which featured various maturities, indicate sustained demand for municipal securities. With offerings like 5s of 2044 at 3.47% and 5.5s of 2049 at 3.62%, there appears to be ample appetite for diverse maturities.

However, the prospect of decreased supply in the coming weeks, compounded by the impending Labor Day holiday and anticipated drop-off in reinvestment cash, might present a backdrop of tightening in the near-term market. Yet, considerable deals remain slated for execution, including the North Texas Tollway Authority’s bonds and the District of Columbia’s offerings.

Looking ahead, market analysts project significant deals which could further shape the market’s trajectory. The upcoming weeks will see issuances from major institutions such as the New York City Transitional Finance Authority and the Texas Transportation Commission. These critical transactions, alongside existing secondary market activity, will be pivotal in dictating the momentum for municipal bond stability.

In a landscape rife with investment uncertainty, the resilience shown by municipal bonds reveals a sector that, while not impervious to fluctuations, has begun to carve a path of recovery. The interplay between municipal and Treasury yields, changes in Fed policy, and robust market activity all contribute to a nuanced understanding of this financial niche.

As we transition into the new month, investors would do well to monitor both macroeconomic indicators and specific municipal developments closely, as these elements will undeniably shape the ongoing viability of municipal bonds as a preferred investment class amidst the oscillating waters of broader financial markets.

Leave a Reply