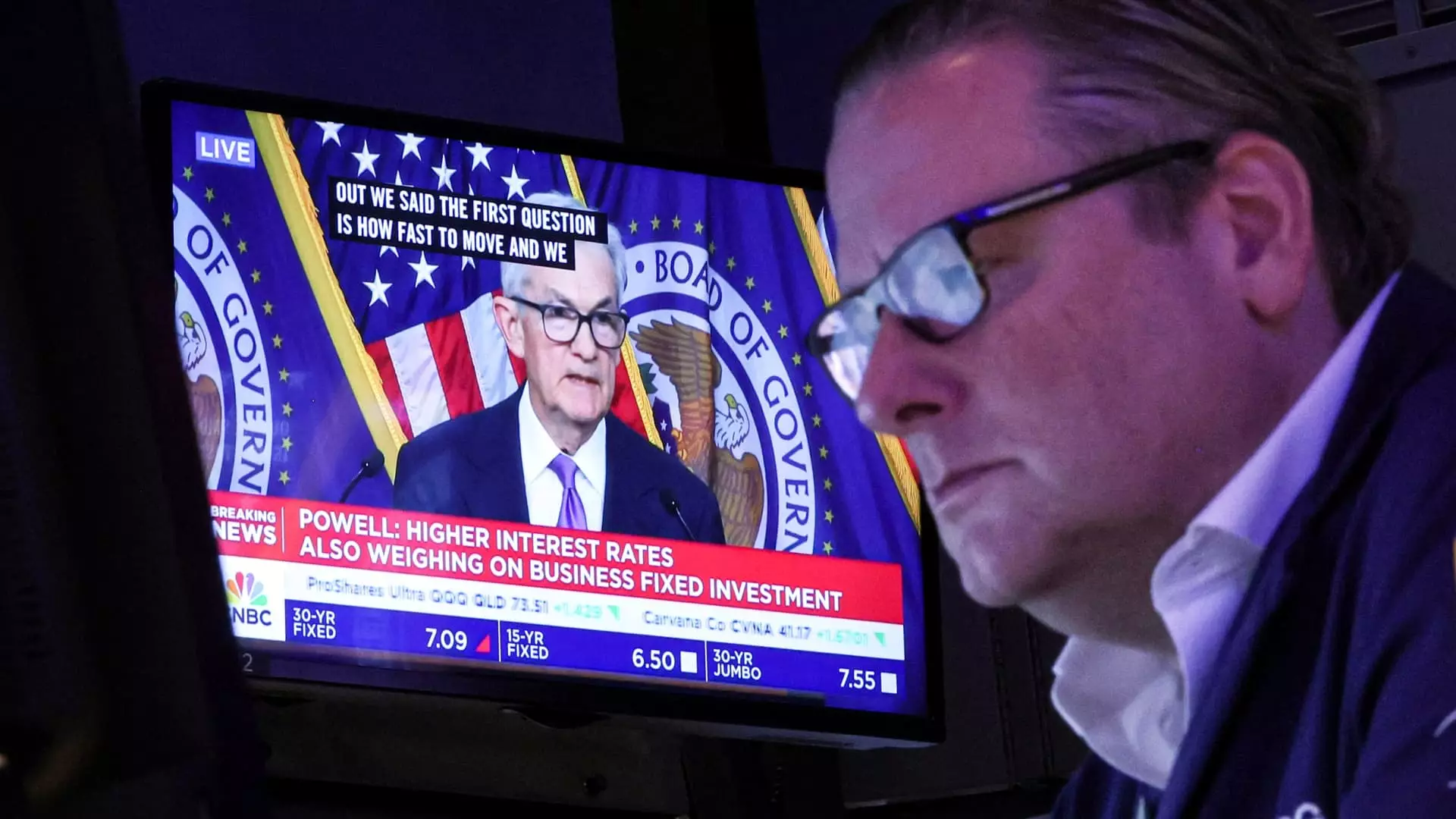

As the Federal Reserve approaches its scheduled meeting on December 18, expectations are rife that a new interest rate cut may occur. This anticipated reduction represents the third consecutive cut, cumulatively reducing the federal funds rate by a full percentage point since the Fed initiated its strategy in September. The persistent economic challenges following a prolonged period of rapid interest rate hikes—implemented to temper inflation, which recently peaked at a 40-year high—prompted the Fed to reassess its policies. Economic analysts suggest that this forthcoming cut might be the last for some time, with caution urged around President-elect Donald Trump’s fiscal strategies as his second term looms.

The federal funds rate is a crucial financial lever controlled by the U.S. central bank, determining the rate at which banks lend to each other overnight. While not directly influencing consumer rates, adjustments made by the Fed significantly affect the broader lending landscape. In light of a likely cut, the overnight borrowing rate could decrease from a range of 4.50% – 4.75% to 4.25% – 4.50%. This potential adjustment is expected to alleviate some financial pressures for consumers, but its effectiveness may vary across different types of loans and credits.

The realm of credit cards is one area where alterations in the federal funds rate are immediately perceptible. A noticeable relationship exists between the Fed’s rates and the average interest charged on credit cards. After experiencing an upward trajectory since March 2022, with average rates climbing to about 20.25%, the anticipated cuts might offer little immediate relief to consumers carrying credit card debt. Card issuers notoriously take longer to adjust rates downward than upward—a lag of up to three months is common. Hence, those struggling with credit card balances should seek alternatives, such as transferring their balance to a 0% interest card, rather than waiting for the Fed’s cuts to trickle down effectively.

Unlike credit cards, the world of mortgages operates quite differently. The majority of mortgages are fixed-rate loans, tied primarily to Treasury yields rather than the Fed’s immediate actions. As of recent reports, the average 30-year fixed mortgage rate hovers around 6.67%, down from previous months but still far exceeding earlier 2024 lows. For homeowners, fixed-rate mortgages mean that any rate cut will not alter their current loan terms unless they refinance, a move that many might hesitate to undertake given the current market rates. Financial experts predict that fluctuations in mortgage rates will persist but remain largely independent of the Fed’s actions.

When examining auto loans, a somewhat parallel scenario emerges. While auto loans can be fixed-rate, consumers face increasingly larger payments due to escalating vehicle prices, which average around $40,000. The average interest on a five-year new car loan stands at 7.59%, a figure that underscores the persistent unaffordability of new cars despite the potential for lower rates. Therefore, even if the Fed enacts further cuts, the realities of high sticker prices and the prevailing economic context will burden borrowers regardless.

Student loans present a unique case, particularly when distinguishing between federal and private borrowings. Federal student loans generally carry fixed rates, making them immune to immediate fluctuations linked to Fed actions. In contrast, variable-rate private loans can respond favorably to interest rate cuts. Nevertheless, students considering refinancing should tread carefully. Transitioning a federal loan to a private one means sacrificing important protective measures such as income-driven repayment plans and potential loan forgiveness.

While the Fed’s rate cuts aim to stimulate borrowing and spending, the underlying economic landscape—characterized by high inflation—complicates this goal. Even with favorable rates in some savings accounts—which now yield close to 5%—the overall necessity for consumers remains unchanged. The financial landscape remains challenging as individuals navigate increasing costs of living, high-interest rates across various lendings, and unpredictable economic policies.

As we look at the potential implications of the upcoming Federal Reserve rate cuts, it becomes evident that the practices of consumers must adapt. While a nominally lower federal funds rate may promise a slight easing of financial burdens, the effects are varied and not uniformly beneficial across multiple borrowing avenues. This scenario underscores the importance of financial literacy and strategic decision-making for consumers in navigating an all-too-complex economic environment.

Leave a Reply