In an era dominated by economic volatility, municipal bonds are often dismissed as stable but dull investment options. However, beneath their seemingly benign veneer lies a complex landscape fraught with strategic significance and inherent risks. As recent market movements indicate, municipal bonds are experiencing a delicate dance of resilience supported by broader Treasury strength, yet the undercurrents hint at vulnerabilities that savvy investors must scrutinize.

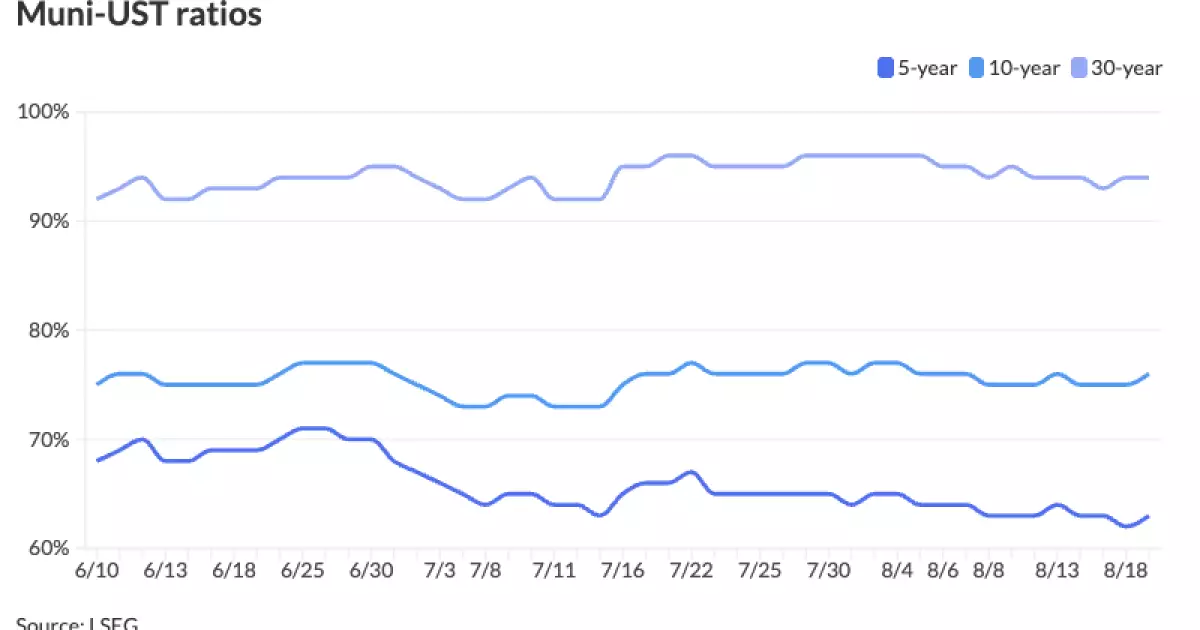

The recent narrow fluctuation in municipal yields amid falling Treasury yields underscores an essential point: the muni market’s strength is not invincible. While a 59-94% muni-UST ratio might suggest an attractive relative valuation—especially with yields hovering at historically low levels—it does not immunize the market from future shocks. The steepening yield curve signals mounting concerns about economic growth and inflation, creating headwinds for longer maturities and lower-rated issuers. It’s precisely this dynamic that warrants skepticism: reliance on short-term Treasury strength as a safety net can be illusory if underlying fiscal health deteriorates or if liquidity conditions tighten unexpectedly.

Moreover, the persistent high issuance — approaching $366 billion year-to-date and forecasted to reach between $575 and $600 billion annually — inflates the supply side pressure, especially considering reinvestment flows are diminishing. The market’s apparent robustness rests on significant reinvestment, an institution-driven phenomenon more susceptible to shifts in federal policy and broader market sentiment. Should these flows wane further due to inflation fears or rising rates, municipal bonds could be exposed to heightened volatility, especially in less creditworthy segments.

Misinterpretations and Overreliance on Market Indicators

Many investors put faith in technical indicators such as yield spreads and credit spreads, but these tools can be deceptive during turbulent times. For example, the widening of spreads without a corresponding decline in actual credit quality can give a false sense of security. Recent signals, like the increased steepness of the yield curve, might be misinterpreted as an opportunity rather than a warning sign. In reality, this steepening reflects investors’ anticipation of economic slowdown and potential fiscal stress in certain jurisdictions.

The market’s subtle shifts in benchmark scales and the marginal fluctuations across different yield curves reveal an illusion of stability. The AAA scales increased slightly, and liquidity seems assured—yet this stability can be ephemeral. Factors like the influence of sector-specific issues, such as the Brightline incident affecting high-yield indices, demonstrate how localized events can cascade into broader sentiment disruptions. The assumption that the retail component remains untouched ignores the possibility of sudden contagion effects or deteriorating credit fundamentals, especially if economic conditions worsen or if fiscal stress manifests unexpectedly.

Furthermore, reliance on broad indices and low granular data might obscure underlying fragility. For instance, while the overall volume of issuance appears healthy, the quality of the underlying credits may be deteriorating quietly. The stable but elevated spreads hint at market complacency—an attitude that can unravel swiftly if fundamental economic indicators, like inflation or Federal Reserve policy cues, shift unexpectedly.

Politics, Public Finance, and the Cost of Complacency

The municipal market’s current state is not just a product of market fundamentals but also deeply intertwined with political uncertainties. Public finance authorities, from city governments like New York to large districts in Texas or Wisconsin, face growing fiscal pressures, which, if mishandled, could impact bond stability. The upcoming primary issuances—ranging from building aid revenue bonds to large school district financings—are indicative of ongoing infrastructure needs and fiscal coping mechanisms. Yet, these issuance waves, if left unchecked or mismanaged amid rising rates, could strain the very fundamentals they rely on.

The danger lies in complacency: relying on recent issuance trends or technical signals to infer long-term stability. Governments and issuers might face credit upgrades or downgrades not just due to immediate fiscal stress but also due to the political will or lack thereof. The political environment in Washington and state capitals can dramatically influence fiscal discipline, which in turn affects bond yields and spreads. Ignoring these underlying macro-political shifts could lead investors astray—especially as some regions contend with hurricane seasons, economic disparities, or mounting debt burdens.

It’s also worth noting that the market’s perception of safety often discounts the long-term cost of fiscal irresponsibility. The current low-interest environment has encouraged states and municipalities to borrow aggressively, risking future fiscal crises if revenues don’t keep pace with their obligations. A shift in federal policy, like fewer expected rate cuts by the Fed, could further complicate the picture, pushing yields higher and exposing the underestimated vulnerabilities of many municipal sectors.

Challenging Assumptions: The Road Ahead for Municipal Investors

Finally, assuming that demand from institutional or retail investors will continue unabated ignores the evolving landscape of risk and return. While large-scale inflows into separately managed accounts and retail demand keep the market buoyant, recent inflation data and geopolitical uncertainties complicate this narrative. If inflation persists or accelerates, the front-end demand that supports muni bonds could weaken, especially as yield premiums become less attractive.

High-yield sectors, such as those impacted by Brightline or other risky financings, are already under stress and could quickly become liabilities if market sentiment shifts. The hazy outlook for future rate cuts and the potential for rising long-term yields suggest that the current slope of the yield curve won’t stay steep forever. For those who dismiss these signals as short-term noise, the risk is clear: the municipal bond market, though seemingly resilient today, harbors vulnerabilities that could explode when investors least expect it.

In this environment, the prudent investor must question the narrative of stability and recognize that the supposed safety of municipals is conditional on continued economic and political stability. The market’s current calm belies deeper issues—issues that, if ignored, could lead to a significant correction and losses for unprepared holders. By critically examining these risks and resisting the allure of complacency, investors can avoid falling into the trap of overconfidence and better navigate the precarious terrain ahead.

Leave a Reply