The municipal bond market, long considered a safe harbor for conservative investors seeking tax-advantaged income, is now revealing unsettling signs of turbulence. Recent data paints a picture of a sector that is not only underperforming but also embodying deeper structural issues that challenge its reputation. Unlike other fixed-income assets that have enjoyed gains, munis—particularly long-dated issues—are suffering significant losses. This divergence from the broader bond universe signals underlying vulnerabilities that demand a critical reevaluation.

One of the most startling features is the stark underperformance of long municipal bonds, especially those with maturity horizons exceeding 22 years. While corporate bonds, Treasuries, and bank loans have thrived, munis have lagged behind, experiencing nearly a 4% decline this year alone. This begs the question: what is causing such a dramatic dislocation? Is the market experiencing an anomaly, or are these signals highlighting a fundamental shift in municipal debt’s risk profile? The answer leans toward the latter, especially given the steepening of the muni curve and the widening spread differentials.

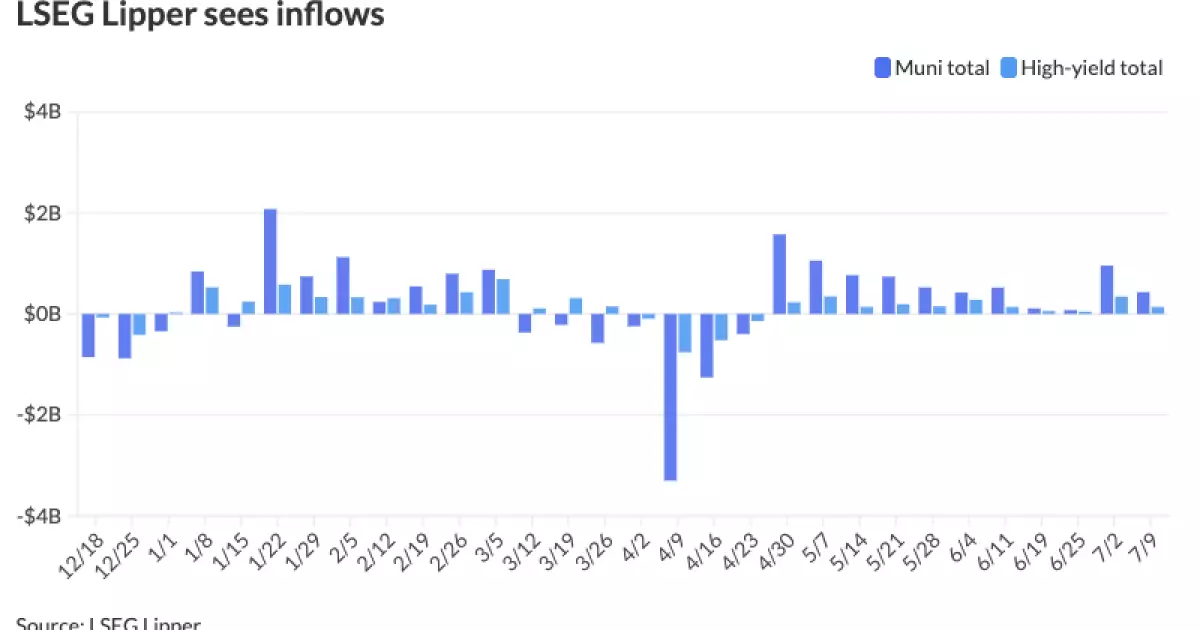

The broader market narrative is complicated by the immense issuance undertaken earlier this year—around $280 billion—driven partly by fears of imminent tax policy changes. Ironically, those concerns proved unfounded, yet the repercussions linger. The induced supply surge, coupled with inflation-driven cost increases on projects and the depletion of pandemic-era aid, has resulted in a perfect storm that has damaged muni valuations. As supply tapers off and the Fed signals potential rate cuts, the market could see drastic shifts, suggesting that current valuations remain fragile and overly pessimistic.

Structural Flaws and Their Manifold Implications

A crucial aspect that cannot be overlooked is the shifting investor behavior and its implications for the muni market’s long-term stability. Institutional investors, such as separately managed accounts and ETFs, exhibit clear preferences—favoring bonds with maturities up to 15 years, wary of the long end of the curve. This de facto preference signals a tilt toward shorter durations, driven perhaps by risk aversion and a recognition of the inherent uncertainties in the extended muni landscape.

This investor bias hints at a potential structural transformation. Is the muni market fundamentally changing, or is this a temporary correction? The evidence suggests the former. The local governments’ borrowing habits are evolving, and the market’s capacity to absorb large issuance volumes may be permanently altered. If long-term munis continue to perform poorly relative to shorter maturities, this could reshape the yield curve and trigger a reassessment of muni risk premiums.

Furthermore, the market’s recent dynamics expose a disconnect between theoretical models and reality. Traditional valuation frameworks underestimated the impact of inflation and debt accumulation on municipal issuers, leading to inflated expectations of safety. The consistent underperformance of super-long munis is a stark reminder that the risks are being underestimated—potentially setting the stage for a more turbulent future.

Political and Economic Factors That Amplify Market Risks

Underlying these technical and structural issues are broader political and economic contexts that threaten to exacerbate muni market vulnerabilities. The recent passage of the tax exemption preservation bill was expected to stabilize the sector, but the damage was already done. The issuance frenzy, driven by tax fears, created an overheated supply environment that may take years to unwind.

Moreover, the fiscal health of local governments remains questionable. Expenses continue to rise amid inflation; aid that once bolstered projects has dried up, leaving many municipalities financially strained. This situation undercuts the perceived safety of municipal bonds, especially for long-term holders. If governments face fiscal distress, the risk of default or restructuring increases—an outcome that savvy investors must seriously consider.

On the macro level, the Federal Reserve’s monetary policy actions will be critical. If rate cuts materialize later this year, they could inject liquidity into the muni market, potentially reversing some of the underperformance. However, this also raises questions about the sustainability of such a rally: will it be a temporary fix, or does it herald a longer-term recalibration of municipal risk premiums? For investors adopting a center-right, liberal perspective—focused on fiscal responsibility and market stability—these questions are more than academic. They underscore the importance of cautious engagement and a recognition that munis are now a more complex asset class than traditionally perceived.

The current state of the muni market should serve as a wake-up call for investors who, until now, regarded municipal bonds as a sanctuary. The heightened volatility, underperformance, and structural shifts expose vulnerabilities that could threaten the safety net that many have relied upon. While the tax-exempt status offers undeniable benefits, it cannot shield investors from the realities of underlying fiscal pressures and market distortions.

To navigate this landscape, prudence must guide decision-making. Relying solely on historical safety margins or complacent about yield premiums is no longer tenable. Instead, investors need a vigilant eye on supply-demand fundamentals, political developments, and macroeconomic signals. The muni market is at a crossroads—its resilience or fragility largely depends on how well market participants understand and adapt to these emerging challenges.

Leave a Reply