The municipal bond market has recently experienced a slight decline for the fourth consecutive day, amidst a backdrop of fluctuating U.S. Treasury yields and advancing equity markets. This scenario indicates a dynamic interplay between these investment vehicles, particularly as municipal yields have seen marginal increases, specifically up to three basis points across various maturities. Concurrently, Treasury yields have escalated by approximately four to five basis points, pushing the two-year U.S. Treasury yield above the psychologically significant 4% threshold for the first time since late August. Such movements underscore an evolving monetary environment characterized by shifting investor sentiments.

The current standing of the two-year municipal-to-Treasury ratio points to a declining relative value in comparative terms: at 61% for two years, 60% for three years, 62% for five years, 67% for ten years, and 84% for thirty years per Refinitiv’s reports. This disparity in yield ratios reflects the broader landscape of municipal credit quality and market demand, prompting professionals to reassess their strategies accordingly.

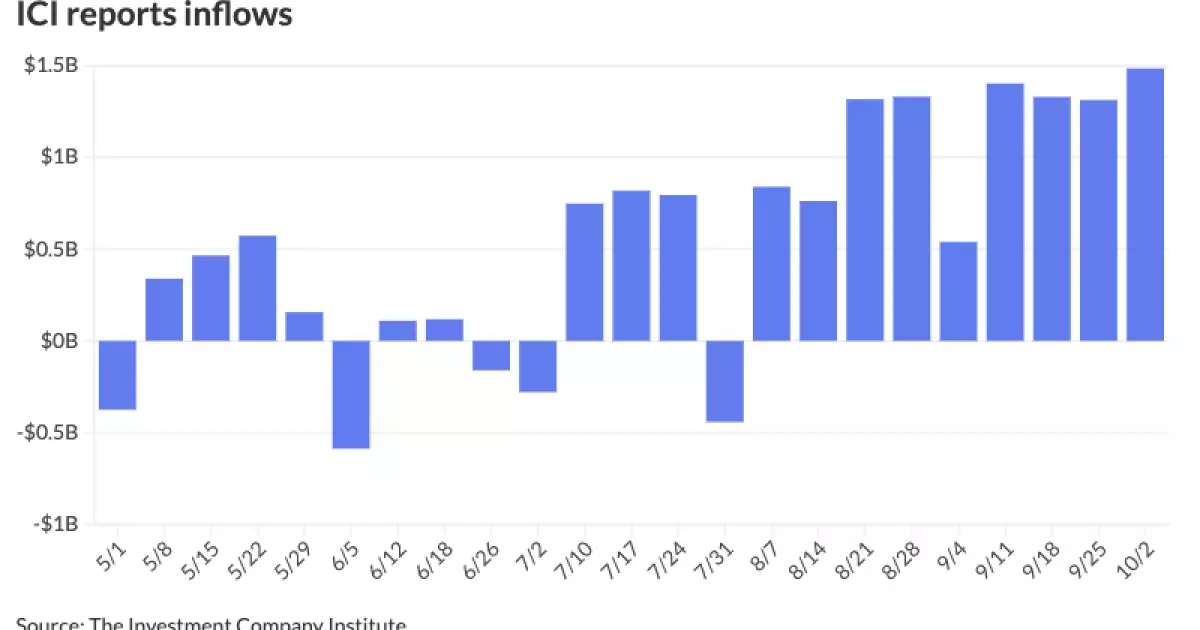

Inflow Trends and Future Outlook

Despite the recent softening in municipal yields, the sector continues to attract capital, as evidenced by robust inflows into municipal bond mutual funds. The Investment Company Institute reported inflows of $1.484 billion for the week ending October 2, marking the ninth consecutive week of positive net flows and a significant uptick from the $1.312 billion the previous week. Moreover, exchange-traded funds (ETFs) have also recorded strong inflows, suggesting a growing appetite for municipal bonds, even as their relative valuations appear strained.

As investor behaviors evolve, some experts, like Jeff Lipton, point to the technical underpinnings that are still driving the municipal market dynamics into 2024. He argues that the market is presently on a “directional footing,” suggesting an anticipatory phase ahead of upcoming policy decisions. With heightened activity in municipal issuance leading up to the presidential elections, there is an observable trend of issuers preemptively positioning themselves to capitalize on favorable market conditions.

The proclivity of issuers to front-load their deals is further reflected in an unprecedented pace of bond issuance exceeding the $10 billion mark on a weekly basis, discounting short holiday periods and Federal Open Market Committee (FOMC) meeting weeks. While this uptick in supply is perhaps indicative of a strategic maneuver to seize tax-exempt financing opportunities before potential shifts in investor sentiment post-election, experts warn that the market may see a temporary subsiding in supply as issuers evaluate market conditions in the latter part of the year.

Despite these fluctuations, analysts assert that the supply should be well digested in the market. Daryl Clements from AllianceBernstein highlights a tendency for investors to exercise greater selectivity, particularly as relative valuations inch toward higher premiums compared to historical norms. As conditions stabilize, potential buying opportunities may arise as ratios recalibrate, offering an attractive entry point for discerning investors.

Calls for Caution Amid Economic Signals

As the U.S. faces macroeconomic pressures, recent economic data has started to underpin the Federal Reserve’s cautious approach toward rate adjustments. Interestingly, while some analysts had anticipated a more aggressive reduction in rates, the market’s sell-off suggests a divergence in opinion between bond market expectations and central bank policy. This ongoing dialogue within the investment community indicates a complex balancing act, where robust demand for munis amidst attractive ratios is pitted against the backdrop of increased yields.

Additionally, it’s important to note that retail investors, in particular, are becoming increasingly attuned to taxable equivalent yield calculations, driving a renewed interest in municipal bonds as a viable investment channel. This shift is vital for the sector, aligning the interests of various investor classes towards understanding and capturing yield enhancements as they navigate this multifaceted financial landscape.

Prominent issuances have dominated the primary market, including a significant $935 million general obligation deal for Connecticut, which saw varied pricing across different series. Such movements highlight the ongoing demand and the capacity of established municipalities to attract capital efficiently. Notable transactions are also underway in broader regions, like Arizona, where BAM-insured revenue refunding bonds are set to price, further showcasing an active primary market despite rising yields.

The current municipal bond market is characterized by a complex interplay of yield adjustments, investor sentiment, and active issuance trends, underscoring the critical need for continued analysis as we approach pivotal economic events, including the impending election. The gradual recalibration of ratios and the sustained inflow of capital into municipal vehicles signal resilience in the face of market fluctuations, presenting both challenges and opportunities for investors in the months ahead.

Leave a Reply