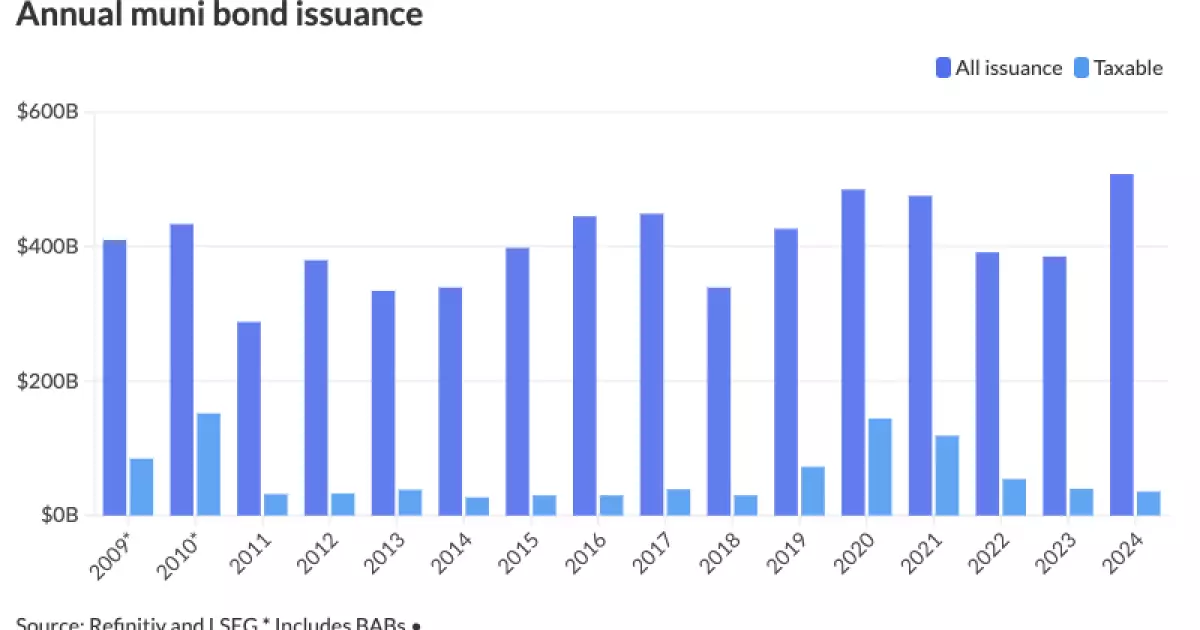

The year 2024 has witnessed an extraordinary upsurge in municipal bond issuance, reaching a record-breaking total of over $500 billion. This significant rise in activity, documented in LSEG data, demonstrates how a confluence of factors—including infrastructure demands, political climates, and major financing deals—has encouraged issuers to flood the market. The $507.585 billion in debt issued this year reflects a striking 31.8% increase from the previous year’s $385.061 billion and breaks the prior record of $484.601 billion set in 2020 by more than $20 billion. These figures highlight a pivotal moment for the municipal finance sector, as it grapples with both heightened demand and complex financial dynamics.

The breakdown of issuance trends reveals intriguing shifts within the municipal bond landscape. Tax-exempt issuance experienced a substantial rise of 36%, climbing to $446.673 billion from $328.536 billion in 2023. Conversely, taxable issuance fell by 10.5%, decreasing to $35.632 billion from $39.817 billion the previous year. Notably, refundings, which allow issuers to refinance existing debt, soared by an astonishing 63.6%, increasing to $84.479 billion from $51.646 billion. New-money volume also rose by 19% to $355.607 billion, demonstrating a robust inclination among municipalities to finance new projects amidst rising infrastructural needs.

The varying trends in tax-exempt versus taxable bonds reveal critical strategic positioning by municipal issuers, especially in the context of evolving market conditions. This juxtaposition has sealed a distinct line between high-demand projects (often financed by tax-exempt bonds) and more discretionary issuances reflected in the decline of taxable bonds.

Initial forecasts for 2024 indicated a conservative range of expectations fluctuations sitting between $330 billion and $450 billion based on considerations such as pandemic-era aid expiration and looming recession fears. However, a shift occurred mid-year when revised projections began to settle into a narrower expectation between $385 billion and $460 billion. This change stemmed from the re-emergence of substantial refunding opportunities and a climate characterized by higher interest rates that, despite their potential to deter issuance, ultimately became a catalyst for robust market activity.

Throughout the year, analysts began to recognize the “Goldilocks” phenomenon—an optimal environment where yields were favorable both for buyers and issuers. Market participants capitalized on this condition, locking in deals before potential disruptions from political uncertainties could impact the climate further. Exceptional liquidity facilitated by mega deals and a favorable reception to large-scale issuances complemented this trend.

Underlying the record issuance is a pressing need for infrastructure upgrades. States and municipalities that had previously amassed cash reserves due to stimulus funds found themselves facing escalating demands as federal assistance dwindled. Urban sprawl and population increases in certain regions—including the ever-growing Southwest and Southeast—have led to intensified infrastructural needs, prompting issuers to finally take their projects to market.

This pressing demand was further reflected in issuance trends, especially in the summer months when municipal bond activity surged. October alone saw a phenomenal figure of $64.643 billion, seen historically as a typical pre-election rush. Observers noted that issuers sought to mitigate future uncertainties linked to the November elections by preemptively securing financing.

Moreover, the increasing frequency and acceptance of mega deals have transformed the landscape of municipal bond issuance. Over the past decade, hesitation to engage in billion-dollar deals has faded, with 2024 showcasing a notable acceptance and demand for larger offerings. These deals not only provide liquidity but also attract a diverse investor base, a sign of confidence in high-value municipal issues.

With projections for 2025 suggesting an issuance range of $480 billion to $745 billion, analysts remain optimistic that the market will either meet or exceed the impressive totals observed in 2024. The potential for changes in tax policy could prompt many issuers to rush to market, seeking to secure favorable rates before legislative changes could influence costs.

As we reflect on specific state contributions, California led 2024 issuance with $71.601 billion, marking a 31.4% increase. Texas and New York followed closely, indicating that key states continue to drive the market. Notably, Florida exhibited remarkable growth, more than doubling its contributions to $27.487 billion, reflecting robust investments in public infrastructure funding.

In sum, the municipal bond market in 2024 is defined not only by record-breaking totals but by evolving dynamics driven by infrastructure needs, political reactions, and a willingness to embrace substantial financial commitments. As we look forward to 2025 and beyond, the lessons learned in this unprecedented year will undoubtedly shape the trajectory and strategies of issuers and investors alike.

Leave a Reply