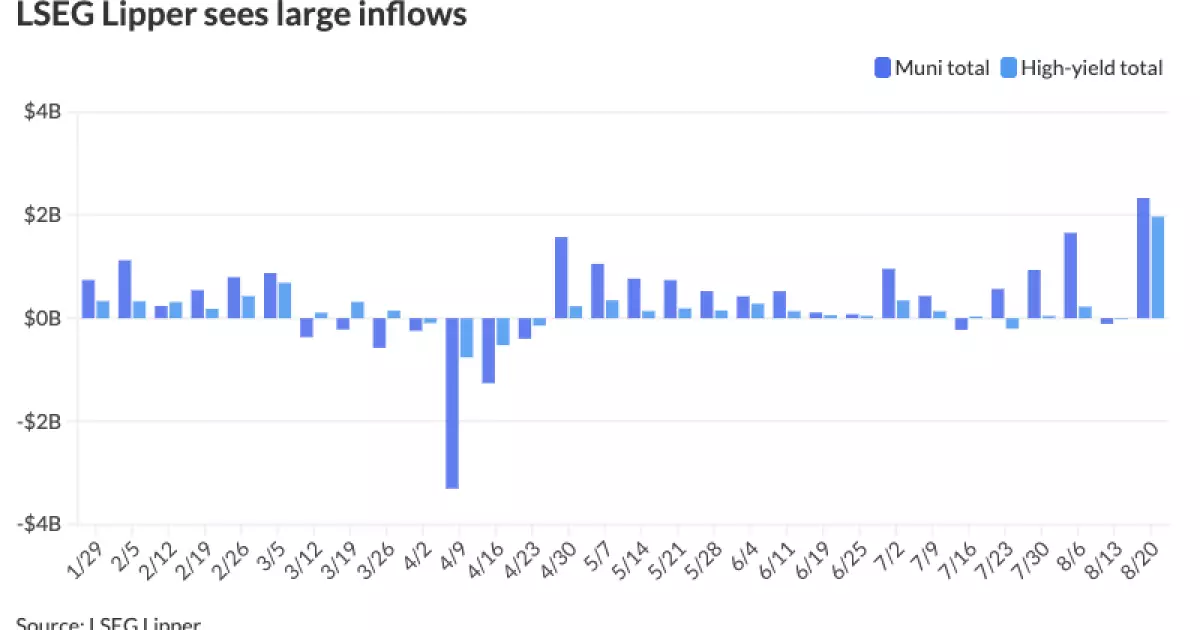

In a surprising twist that defies the usual calm of municipal markets, recent data reveals a significant influx of capital into municipal bond mutual funds—over two billion dollars in just one week. This sharp rebound, the largest in over two years, lures investors into believing the municipal sector is resilient and perhaps undervalued. However, this optimism may be misplaced, as it obfuscates underlying fragilities and the broader economic tensions at play. The surge, driven heavily by high-yield funds and ETF reallocation, suggests not genuine confidence but opportunistic chasing of yield in an ever-uncertain macroeconomic environment.

What stands out is the concentration of inflows into specific high-yield ETFs, notably the Capital Group Municipal High-Income ETF, which commanded a $1.5 billion influx. Such concentrated movements often signal tactical reallocations rather than long-term trust. It raises questions about the stability of the fund flows—are these solid bets or just short-term predatory positioning as investors try to capitalize on fleeting market noise? It’s a classic case of “emotional investing” overcoming fundamental analysis, especially when one fund’s single large inflow accounts for over three-quarters of the mental picture.

This scenario echoes the paradox of a market that appears lively on paper yet is fraught with risks beneath the surface. The municipal bond sector, long considered a safe harbor, now finds itself riding a wave of technical inflows that may not be sustainable. While the overall market seems steady, what we are seeing is a fragile veneer that could crack under the weight of upcoming economic realities: rising UST yields, possible rate cuts, and the inevitable fiscal pressures that local governments face.

Market Dynamics and the Shadow of Uncertainty

Looking beneath the surface, the municipal market’s technical signals reveal an unsettling duality. On the one hand, secondary market trading volumes remain steady, indicating some underlying liquidity. On the other hand, municipal money market balances are at their lowest levels since mid-April, hinting at investor wariness. The withdrawal from money markets, combined with yields slightly above fixed coupons, further emphasizes that many investors are contemplating exit strategies or at least reassessing risk thresholds.

The bond yield landscape adds to this ambiguity. The muni-UST ratios—the comparative measure of municipal bond yields against U.S. Treasuries—hover near historically high levels, suggesting munis are relatively attractive but also hinting at looming divergences. The 30-year ratio pushing toward 94-95% indicates municipal bonds are pricing in a premium, but it also warns of potential overextension should UST yields continue to rise or if the Fed signals a pause or reversal of rate hikes.

Indeed, the upcoming Federal Reserve policy decisions cast a long shadow over this fragile calm. With market sentiment oscillating between expectations of a rate cut and fears of another rate hike, municipal investors face a treacherous landscape. A rate cut, while seemingly supportive, could lead to a rush for income as yields plummet, destabilizing the current inflows. Conversely, if rates hold firm or rise, munis may suffer from diminished appeal, especially if investors recalibrate towards safer, more liquid assets.

Alarmingly, historical patterns reveal that September has often been a turbulent month for fixed income markets, with average losses of over 1%. This seasonal weakness, combined with the Fed’s delicate balancing act—trying to tame inflation without triggering recession—means the municipal sector’s seemingly resilient prices could be short-lived. The market may be sleepwalking into a correction, hinged on overly optimistic assumptions about Fed policy and fiscal stability.

Fiscal Prudence or Reckless Optimism?

The primary market action provides further insight into the current environment. Large bond issuances, such as Montana’s $111 million deal and Louisville’s $234 million water bonds, demonstrate confidence from issuers but also risk overstating demand. These deals are priced at relatively modest yields, but the risk lies in whether investors are truly willing to hold long-term bonds if the economic backdrop shifts sharply.

The broader trend points to a cautious optimism that may soon be challenged by reality. Despite the influxes, the municipal sector’s underlying fiscal health remains a concern. Over-leveraging, pension liabilities, and infrastructure needs continue to weigh on local governments, often leading to a false sense of security among investors who chase yield without appreciating the underlying risks.

Meanwhile, the declining number of identity requests for new municipal securities—down 10.4% compared to June—might hint at a cautious stance from underwriters and issuers, possibly foreshadowing a slowdown or correction ahead. The variation in yield curves across different data sources and models highlights the uncertainty that currently pervades bond valuations.

In the final analysis, the apparent strength of the municipal market is a mirage born of technical factors and short-term inflows. It is a mirage that could fade quickly once market sentiment shifts, interest rates rise, or the fiscal realities of municipalities become too glaring to ignore. The ongoing debate about the Fed’s next move encapsulates this precarious situation: a fragile equilibrium teetering on the edge of upheaval that could challenge the sector’s perceived safety and value.

Leave a Reply