The municipal bond market has shown a slight strengthening in specific areas, contrasting with the movements of U.S. Treasury yields which have continued to dip. As the Treasury market experiences fluctuations, the municipal-to-Treasury ratios reveal intriguing patterns that signify a mixed response from investors. According to recent data from Municipal Market Data, the ratios for various maturities—62% for two-year bonds, 64% for five-year, 68% for 10-year, and 87% for 30-year bonds—suggest a relatively stable environment for municipal bond investors. This environment is crucial, especially as demand for stringent fiscal policies has been rising due to inflationary pressures and increasing construction costs, which are compelling municipalities to seek financing for infrastructure projects.

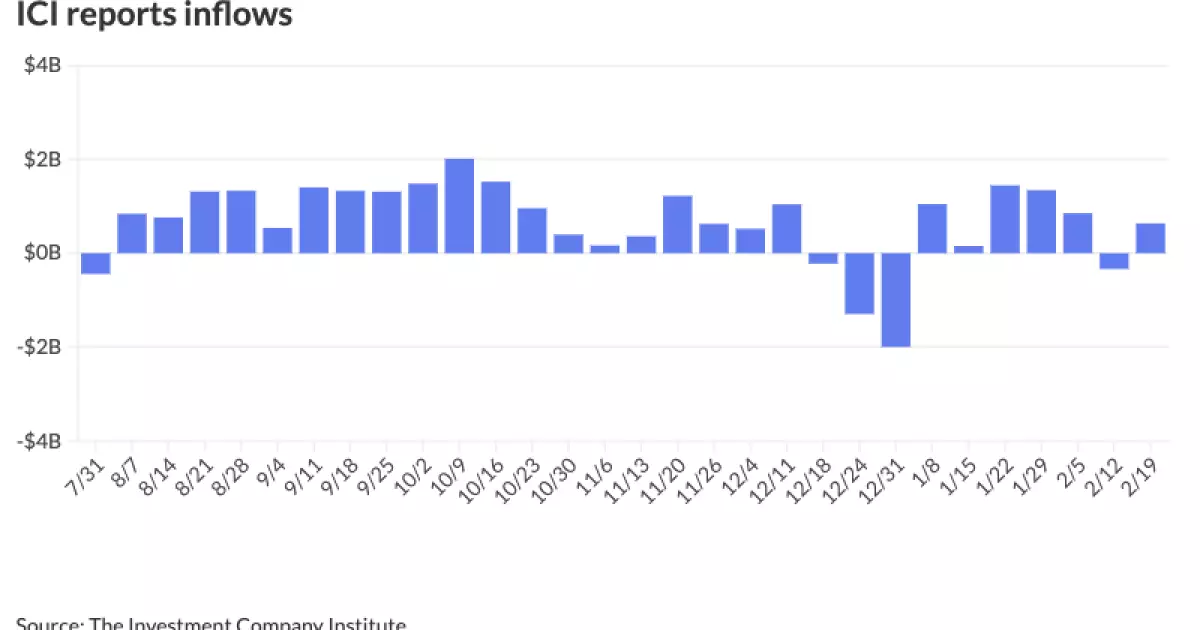

In addition to the shifting demand dynamics, the recent report by the Investment Company Institute indicated a strong inflow of $635 million into the municipal market for the week ending mid-February, a significant turnaround from the $336 million outflow of the previous week. Moreover, exchange-traded funds (ETFs) saw substantial inflows of $782 million, suggesting that investor confidence is regaining ground after a tumultuous period in the market.

The entry of numerous issuers into the municipal realm—characterized as a “heavy start” by municipal research analyst Jeff Devine from GW&K—indicates a strategic move to capitalize on favorable market conditions before potential changes to the tax exemption that encourages municipal financing. Municipalities are not only motivated by the desire to secure funding for long-deferred infrastructure projects but are also responding to inflation that has inflated construction costs significantly.

The trend of increasing issuance can be attributed to several mega-deals, with the South Carolina Public Service Authority recently completing a notable $1 billion bond sale. As highlighted by Jeff Timlin from Sage Advisory, February’s market is expected to offer relative stability concerning the supply and demand dynamic. However, the following months may experience a shift, with a decrease in anticipated coupons and maturities, urging investors to remain vigilant.

Policy discussions surrounding the potential elimination of the municipal bond tax exemption continue to loom large in the background. Timlin emphasizes the nuanced aspects of this debate, pointing out that while the cost to the federal government from this exemption could be significant, the broader societal benefits—like improved public services and infrastructure—are crucial to consider.

The impact of eliminating this exemption would be profound; it would increase borrowing costs for municipalities and compel them to enhance revenue through alternate means—likely leading to higher taxes. However, Devine suggests that the complete abolishment of this exemption is unlikely, citing historical tendencies where lawmakers consistently discuss adjustments without outright elimination, like the eliminated advanced refundings in 2017.

In the volatile landscape of municipal finance, there are indications of progressive development regarding the future of the tax exemption. Reports suggest that House members might be more amenable to using scoring methods favored by Senate Republicans, which could pave the way for permanent extensions of the exemption without encountering significant fiscal hurdles. However, proposals such as raising taxes on university endowments indicate that certain market sectors—especially higher education—remain at risk of being adversely affected.

As we delve deeper into specifics, the primary market has recently witnessed several significant transactions. For example, Bank of America Securities issued a notable $950 million of revenue bonds for the New York City Municipal Water Finance Authority, and Jefferies managed the pricing of $346 million in general fee revenue bonds for Auburn University. Furthermore, notable competitive sales, such as those for the Springfield Board of Public Utilities and Hoboken, New Jersey, serve as markers of the diverse and dynamic nature of municipal financing.

Economic indicators suggest that the market remains attentive to Treasury movements, with recent reports reflecting a slight firmness. This responsiveness underscores the importance of monitoring yields closely, especially as they fluctuate amid various economic factors.

Overall, the municipal bond market stands at a critical juncture marked by a mix of stable inflows, fluctuating issuance rates, and impending policy implications. Investors must navigate these waters carefully, gauging the impact of both current market conditions and potential legislative changes that could redefine the landscape of municipal finance. As municipalities forge ahead seeking to address their infrastructure needs amidst inflationary challenges, understanding the market’s pulse will be essential for stakeholders looking to capitalize on opportunities while mitigating risks.

Leave a Reply