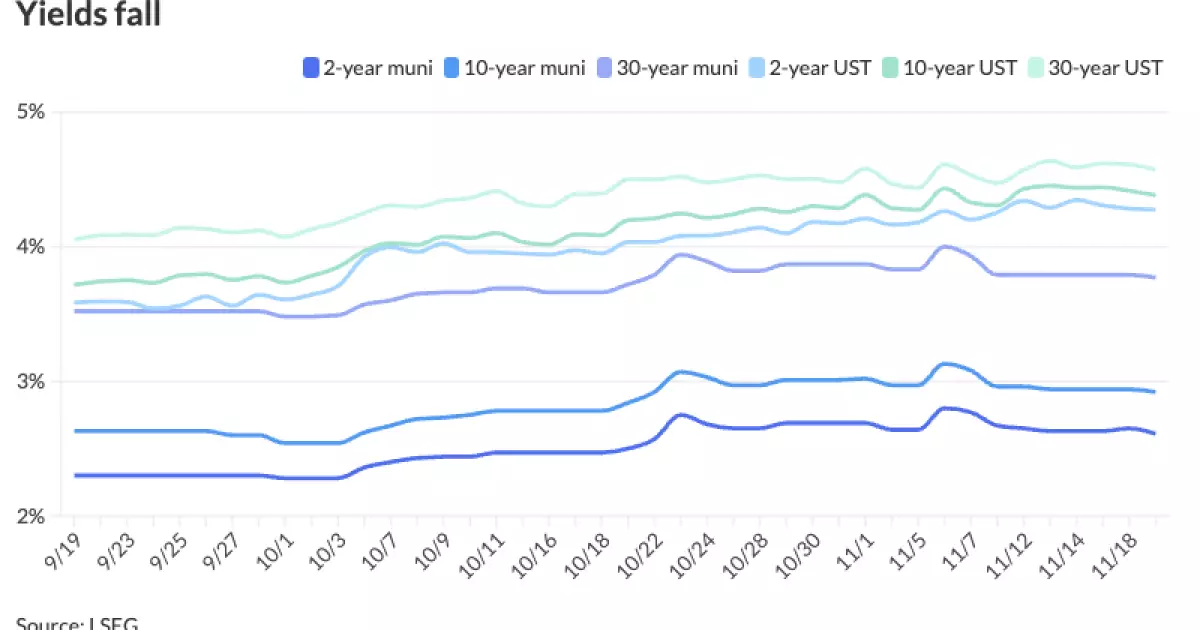

The municipal bond market has recently demonstrated resilience amidst fluctuating U.S. Treasury yields and a mixed performance in equities. This stability is noteworthy, especially considering the significant movement in U.S. Treasury (UST) rates, which have experienced slight declines, offering a contrasting trend to the overall volatility seen in stock markets. Notably, it was reported that yields on Triple-A municipal bonds improved, rising between one to six basis points along different points on the curve. This adjustment reflects a broader sentiment of cautious optimism within the municipal finance sector.

As the market adjusted, a shift in focus from the secondary trading space to primary issuances became apparent. Several high-profile transactions were executed, most prominently the $1 billion financing for the United Airlines Terminal project in Houston, which attracted substantial investor interest. Industry insiders, like Chris Brigati from SWBC, suggest that although the upcoming issuance calendar appears less busy compared to the weeks leading up to the election, the current situation still offers a reasonable supply environment. The key takeaway from Brigati’s commentary is that strong pent-up demand has led to tight market conditions, making it increasingly challenging for investors to find available paper.

The performance of municipal bonds, particularly in the short-term, highlights their attractiveness amid an uncertain economic landscape. According to Matt Fabian of Municipal Market Analytics, the ratios, especially for shorter maturities, have reached exceptionally favorable levels. For instance, the two-year municipal to UST ratio stood at 61%, while other maturities reflected similarly compelling figures. This impressive performance underscores a growing preference among investors for quality yields, particularly as retail sentiment pivots towards better income prospects.

The dynamics of retail investor involvement tell a compelling story. With trade counts in the municipal bond market surpassing 300,000, much of the retail demand has been directed through separately managed accounts. This trend suggests a robust appetite for income-generating assets among retail investors, driven by favorable yields. Additional insights from Fabian reveal that mutual funds and ETFs have experienced modest inflow trends, while money market funds have faced outflows, likely accounting for transient cash movements among investors.

Interestingly, the sustainability of this positive momentum within mutual funds remains to be seen as the year progresses. In 2023, it is anticipated that mutual funds could witness a total inflow of $30 billion, which would make for one of the stronger years in the past 15. However, the ability of these funds to maintain this pace is contingent upon future market conditions, including supply levels and interest rate movements.

Looking ahead, the landscape for municipal bond supply appears to be influenced by several factors, including the impending threat to tax exemptions. Historical comparisons indicate that the closing weeks of the previous year saw significant issuance, totaling $45 billion. In contrast, 2023’s issuance trends suggest that, barring unexpected declines in yields, the full-year supply could approach or even breach the $500 billion mark, building upon the already impressive $451 billion in issuance recorded in just 46 weeks.

Fabian’s analysis indicates that the trajectory of yields will be pivotal in determining future supply dynamics. Should UST yields experience notable declines, reactions in the municipal bond market might prompt additional price contractions or yield hikes, particularly in response to inflation and credit concerns.

In practical terms, the recent actions in the primary market showcase a variety of notable issuances. For example, BofA Securities successfully priced $1.1 billion in United Airlines Terminal Improvement Projects bonds, adjusting yields upward by five to 15 basis points. Concurrently, Goldman Sachs facilitated the pricing of green revenue bonds for California’s Community Choice Financing Authority, promoting sustainable investment strategies.

Further, various states are actively managing local finance needs, with upcoming issuances scheduled for educational projects in Arizona and infrastructure projects across the country. This confluence of activity signifies a broader trend where municipalities are not only responding to immediate financing requirements but also aligning their strategies with investor preferences for environmental governance and infrastructure resilience.

As the municipal bond market navigates a complex landscape marked by fluctuating yields, varying demand levels, and a potential influx of supply, stakeholders remain vigilant. The resilience demonstrated in recent market behavior, coupled with favorable yield conditions, underlines the attractiveness of municipal bonds as a stable investment avenue. The coming months will be pivotal in determining how these trends unfold, emphasizing the need for continuous monitoring of market indicators and investor sentiments.

Leave a Reply