The recent landscape of the municipal bond market has displayed a slight decline, particularly evident on a Wednesday when investor sentiment was notably affected by the larger weaknesses observed within U.S. Treasury securities. Nevertheless, municipal bonds have continued to demonstrate resilience, managing to outperform Treasuries despite the overall softness. A crucial focal point for investors during this period has been the primary market, where several sizable new issues appeared, underscoring a robust demand even amidst a backdrop of fluctuating yields.

While the yield curves for Triple-A municipal securities displayed marginal changes, they typically saw declines ranging from one to four basis points across various maturities. In stark contrast, the Treasury market experienced more substantial losses, particularly for longer-duration bonds. Consequently, the ratios comparing municipal securities to Treasuries have adjusted downwards, revealing implications about relative value perceptions among investors.

The sell-off in Treasuries has not diminished the enthusiasm for new municipal bond issues. According to market experts, including Julio Bonilla from Schroders, the demand for new municipal bonds remains “incredible.” This optimism is supported by significant liquidity in the market, evidenced by the staggering $6 trillion held in money market funds and an additional $2.5 trillion in certificates of deposit. High liquidity is a key driver that pushes institutional and retail investors towards the municipal market, especially when the relative yields appear attractive after tax considerations.

As the Federal Reserve approaches potential rate cuts, investors are increasingly seeking to capitalize on long-term bonds. Numerous marginal investors are testing the waters as they contemplate transitioning funds away from shorter instruments, driven by the allure of locking in yields at better rates for the long term. This trend further fuels the sentiment in the muni market, which benefits significantly from the liquidity influx.

Recent Municipal Issuance: A Closer Look

On a notable day for the primary market, Columbia University entered with a substantial $500 million offering comprising both taxable corporate CUSIPs and revenue bonds. The pricing of these bonds came with tight spreads, indicating a strong demand and confidence from investors. Similarly, other issuers like the Kentucky State Property and Buildings Commission and Massachusetts made significant offerings, illustrating the broad appeal and operational stability across various sectors of the muni market.

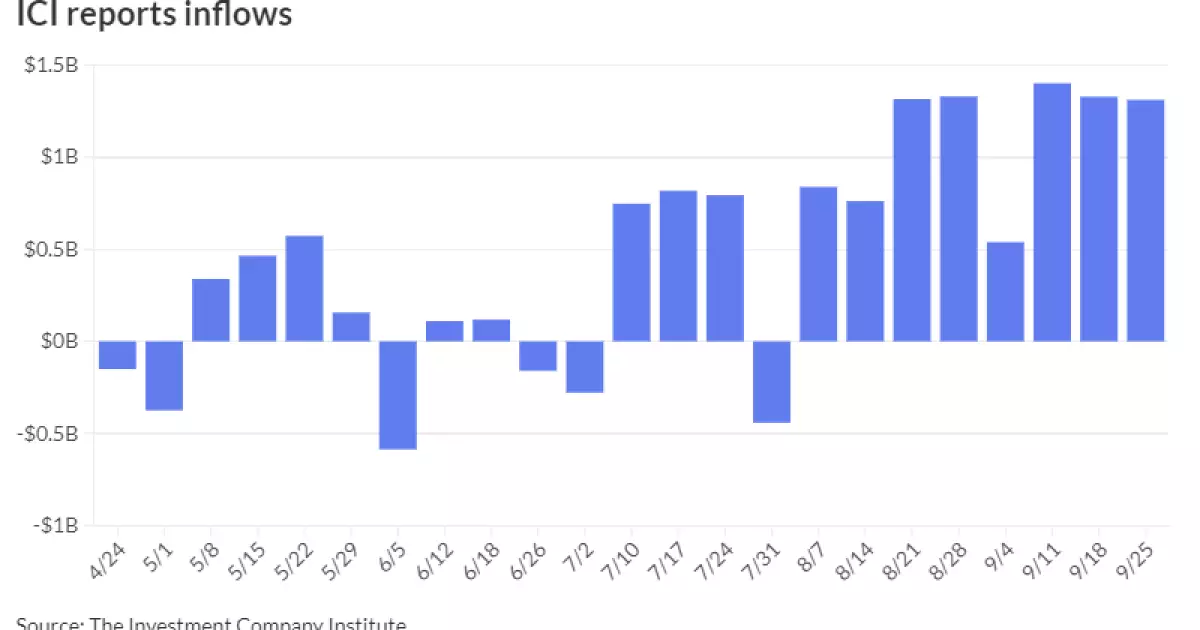

The enthusiasm surrounding these new issues is critical for sustaining momentum moving forward. This is evidenced by the recent statistics from the Investment Company Institute, which reported inflows surpassing $1.3 billion into municipal bond funds. The steady stream of capital reflects investor confidence and a pivot towards securing relatively stable yields in the face of impending rate changes.

Implications of Investor Behavior on Market Activity

Investor behavior remains a pivotal factor influencing the municipal bond landscape. The notable uptick in fund trading activity, which encompasses approximately 275,000 total trades recently, has raised questions regarding the consistency of bank demand. With the Federal Reserve’s well-documented slow approach towards increasing rates, the expectation for further engagement by retail investors suggests a potential rally in the municipal market.

Looking ahead, should the market witness a rally, year-end refundings may generate an increase in issuance. This scenario could position the 2024 issuance figures to challenge previous records, reflecting sustained retail demand across various bond categories.

Analyzing how the yield curve has shifted, various data points illustrate a nuanced stability within the municipal sector. According to Refinitiv Municipal Market Data, the one-year yields remained unchanged, ensuring consistency in an otherwise volatile landscape. This stability across different maturities showcases the robustness of municipal bonds, particularly as actuaries consider longer-term financial commitments amid growing inflation expectations and supply chain uncertainties.

In comparison, the Treasury market has exhibited pronounced increases in yield across all tenors. For instance, the two-year yield crested at 3.635%, highlighting a marked premium that Treasuries now command over comparable municipal yields. This rise in Treasury rates relative to municipal offerings has contributed to an evident preference among some investors leaning towards municipal bonds, chiefly due to their typically more favorable tax adjustments.

The municipal bond market is currently navigating a period characterized by market fluctuations, strong investor demand, and high liquidity. The delicate balance between municipal bonds and Treasuries presents a unique opportunity as investors look for better-structured long-term investment solutions. The robust inflow of funds and recent issuance activity suggest a continuing positive sentiment, positioning the municipal market favorably as it heads toward the end of the fiscal year and beyond. As market dynamics unfold, investors must stay vigilant to leverage opportunities presented by ever-changing conditions while strategically aligning their portfolios.

Leave a Reply