As we navigate the complex landscape of municipal bonds, several key factors emerge that highlight both current trends and future implications. With recent movements in U.S. Treasury yields and market dynamics impacting municipal finance, a clearer understanding of how these elements interact is essential for investors and analysts alike.

In the most recent trading sessions, municipal bonds demonstrated a slight increase in strength as U.S. Treasury yields experienced a decline. This relationship is vital, as movements in Treasury yields often correlate with shifts in the municipal market. On this particular Monday, yields on municipal bonds were nudged upwards by four basis points in various maturities. In contrast, U.S. Treasury yields decreased by five to nine basis points, particularly showing the most significant declines in shorter maturity bonds—specifically those under ten years.

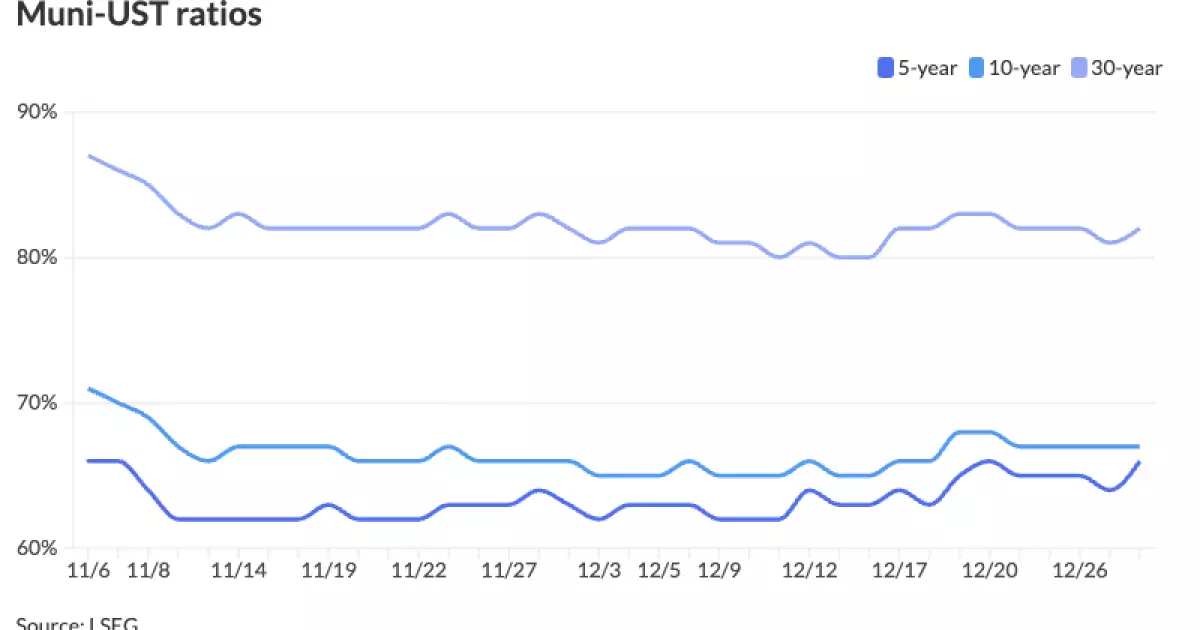

Analysis of the municipal-to-Treasury yield ratio reveals some consistent patterns. For instance, the ratios remained relatively stable, with two- and five-year ratios both hovering at 66%, a stable measure indicative of how municipal rates are responding to Treasury yields. This data is crucial, as it provides insight into relative pricing between municipal bonds and their taxable counterparts. Year-to-date statistics further illustrate the municipal bond market’s resilience, with a return of +0.73% compared to a modest +0.23% for U.S. Treasuries in the same period.

Looking toward the future, investment-grade municipals are expected to face challenges. Barclays strategist Mikhail Foux noted that these indices entered 2024 at notably rich levels, posing a risk as there is limited cushioning against sudden changes. Notably, the performance of investment grades saw significant strain as U.S. Treasuries sold off in December, which pushed down year-to-date returns amidst increased volatility.

This continued underperformance can be attributed to heavy issuance and tepid demand from institutional investors. In December, high-yield bonds experienced a loss of -1.97%, but their overall returns for 2024 remained robust at +5.98%. It’s also essential to understand that high-yield assets are currently in a position to absorb rate volatility better, potentially granting them an edge over less flexible investment-grade counterparts.

Another reiteration from Foux suggests that both high-yield and investment-grade indices will likely end the year with richer yields compared to U.S. Treasuries, indicating a need for investors to be cautious about their strategy moving forward, particularly with regard to rate fluctuations.

One of the looming concerns facing the municipal finance market is an anticipated surge in supply, projected between $450 billion to $500 billion for the upcoming year, driven by the need for critical infrastructure updates and the exhaustion of pandemic relief funds. Portfolio manager Jeremy Holtz expressed that this increased supply aligns with an environment where demand for tax-exempt yield is already substantial, posing headwinds as the market prepares to absorb

Leave a Reply