The municipal bond market has demonstrated an environment of resilience, marked by modest shifts in yields and a shift in investor sentiment as we transition into the new year. As the bond calendar opens with an impressive influx of supply and an anticipated uptick in market activity, the atmosphere is ripe for both opportunity and caution. This article delves into the recent developments in the municipal bond market, dissecting the latest yield trends, investment opportunities, and the broader implications of forthcoming economic indicators.

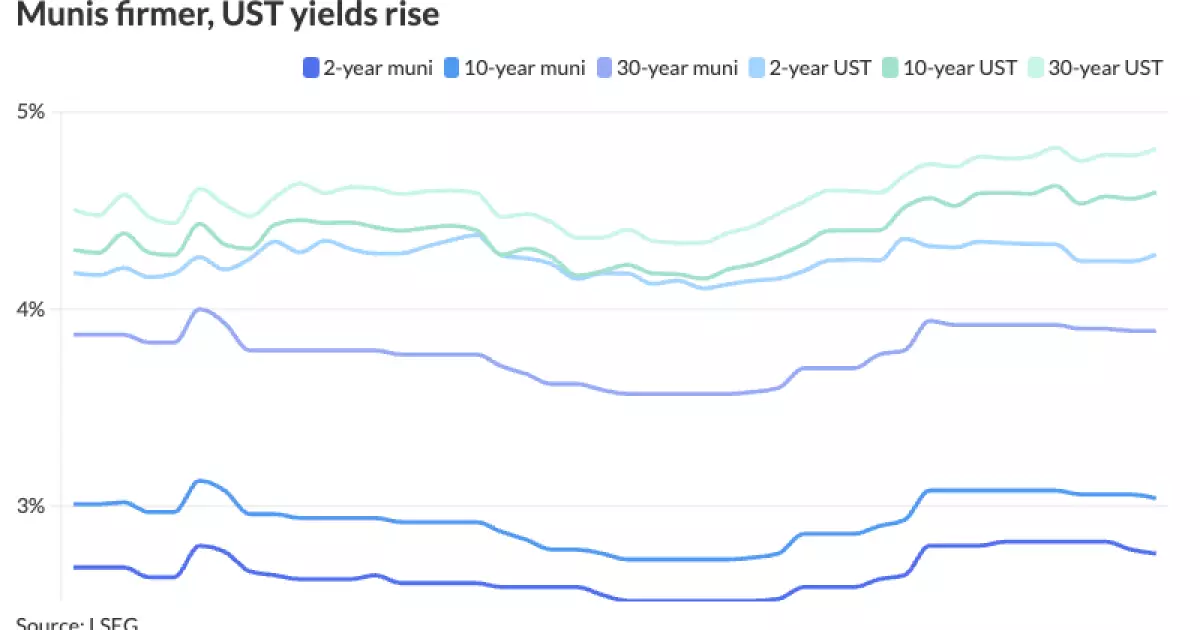

The start of the year has witnessed a tightening of municipal yields, with Triple-A rated bonds witnessing reductions of up to seven basis points primarily in the short-term segment. In stark contrast, U.S. Treasury yields have observed a slight uptick, reflecting a broader context of investor behavior and economic expectations. According to Mikhail Foux, managing director at Barclays, the trend of rising municipal yields last month—with increases over 30 basis points—has adequately positioned many municipal bonds to appeal to a wider array of investors.

While December’s performance did not culminate in the anticipated year-end rally, Foux expresses a tempered optimism as supply dynamics appear critically subdued. Presently, the 30-day visible supply is resting at just shy of $10 billion—a significant indicator that could steer market behavior in the immediate future. This combination of lowering yields on municipals and rising supply levels means investors may find favorable pricing despite the overall prospect of higher interest rates.

A substantial week looms ahead for the municipal bond market, with a healthy issuance of over $5 billion expected, led by notable transactions like the $1 billion revenue bond offering from the Southeast Energy Authority. This influx of new issues is crucial, particularly given the current environment of heavy redemptions and coupon payments expected within the month, a factor that may stabilize pricing and demand in the market.

Additionally, key transactions poised for execution include $850 million in general obligation bonds from the San Diego Community College District and $144 million of GO school project loan chapter 70B bonds from the Tri-County Regional Vocational Technical School District. These substantial offerings are not merely a reflection of immediate capital needs; they indicate strategic moves aimed at long-term infrastructure investments that resonate well with investor sentiments seeking steady returns in a volatile market.

January is traditionally a month characterized by heightened redemption activity, anticipating an outflow of $16.3 billion against the provided interest obligations. Notably, states like Illinois, Texas, and New Jersey are at the forefront of this redemption wave, each accounting for billions in redemptions. Such liquidity movements are essential as they dictate the short-term health of the municipal bond market and its capacity to attract fresh investments.

Foux posits that while there is some skepticism surrounding the market’s performance, the trend observed in early January may be influenced by seasonal factors rather than a long-term bearish stance. Historical data suggests that January performance has often varied, with some years yielding substantial gains whereas others have tested investor resolve through considerable losses.

As professionals in the market prepare for potential shifts in fiscal policy and regulatory changes under the new administration, the environment is charged with uncertainties. Wong points out that the federal government’s monetary policy will directly impact investor willingness and overall supply levels. In the first quarter of the year, expectations for a potential pause by the Federal Reserve could provide a stabilizing effect on the market as it navigates through persistent inflationary pressures and robust employment figures.

Moreover, despite the notion that municipal bonds remain relatively expensive compared to yield benchmarks, key ratios signal that these investments may still hold significant value for many investors. The two-year municipal to UST ratio at 65% and the creeping ratios across longer terms indicate that, while these bonds might be perceived as pricey, the historical context places them favorably in the risk-return evaluation.

The landscape of the municipal bond market as we enter the new year presents a combination of challenges and prospects for investors. With fresh supply entering the market, a significant influx of redemptions, and shifting yield dynamics, stakeholders must remain vigilant. Market strategies will depend not only on interest rate movements but also on broader economic trends coming from influencing policy changes. Thus, while January traditionally characterizes a fluctuating performance in the muni bond market, the ultimate key will be striking a balance between caution and opportunity as the year unfolds.

Leave a Reply