In a recent market development, municipal bonds showed signs of resilience, outperforming slight losses experienced in U.S. Treasuries on Tuesday, while both the Dow Jones Industrial Average and the S&P 500 achieved record highs. This uptick comes on the heels of the Federal Open Market Committee (FOMC) meeting, where minutes indicated that the Federal Reserve would adopt a cautious approach regarding future monetary policy adjustments. The sentiment from the meeting underscored a potential long-term move towards a more neutral stance, contingent on the economic landscape progressing as anticipated. Priscilla Thiagamoorthy, a senior economist at BMO, emphasized that there is no immediate urgency for rate cuts, aligning with the anecdotal support for a gradual easing of monetary policy among Fed officials.

The municipal market demonstrated robust strength on Tuesday, with triple-A yield curves experiencing a dip in yields of up to five basis points. In contrast, U.S. Treasuries faced a decline of up to four basis points. Matt Fabian from Municipal Market Analytics noted a marked improvement in the distribution of municipals to retail investors through separately managed accounts, which has contributed to a more expansive market base. Although the prior week’s fixed income showings resulted in only a modest net rally, demand for municipal bonds, particularly among retail investors, surged as they geared up for year-end buying amidst a predominantly quiet holiday calendar.

Interestingly, the broader atmosphere in the Treasury market seemed to be characterized by a mixed sentiment in response to global events—most notably the intensifying conflict in Ukraine, which drew investors towards safe-haven assets. The prevailing thought among analysts is that while Treasuries may see softness in the upcoming weeks, municipal bonds could continue to flourish thanks to their relative stability and resilience.

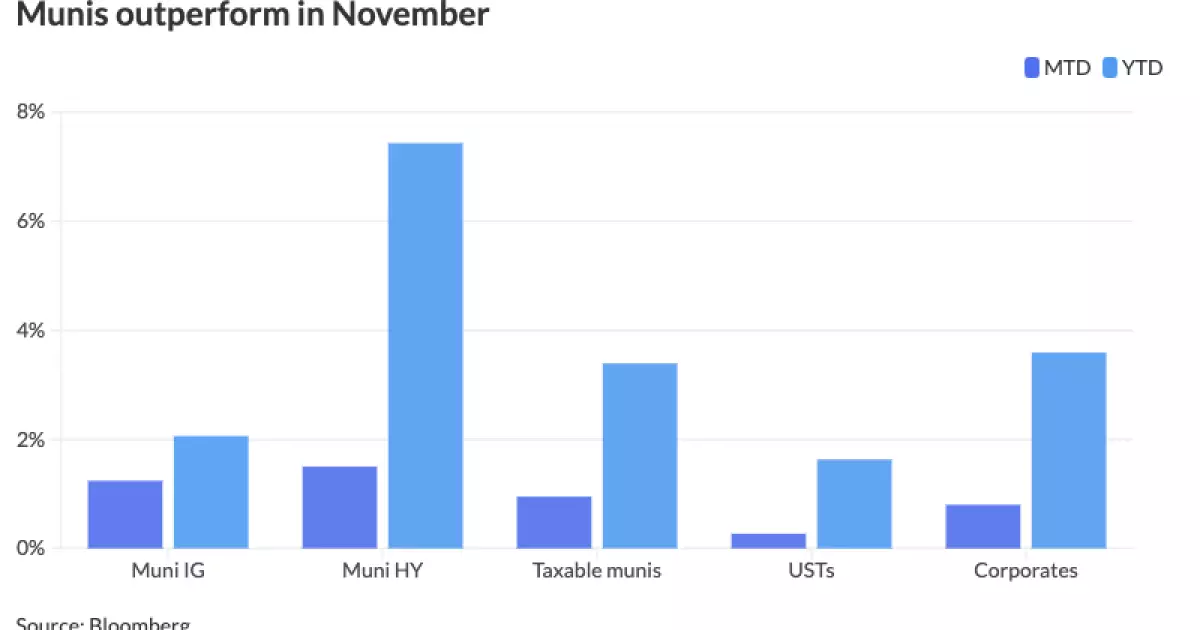

In terms of performance, municipals have recorded a return of 1.24% in November and an impressive 2.06% year-to-date as reported by the Bloomberg Municipal Index. High-yield municipals similarly fared well with gains of 1.50% month-to-date and a 7.43% increase year-to-date. Taxable municipals have not lagged behind, posting returns of 0.95% for November and 3.39% for the year thus far. Comparatively, U.S. Treasuries showed more modest growth, with November returns of 0.27% and a year-to-date gain of 1.63%.

A notable measure of performance is the ratio of municipal bonds to USTs, which is a critical indicator for investors. As of Tuesday, this ratio stood at 61% for two-year maturities, climbing to 82% for 30-year maturities. These ratios not only reflect the value perception of municipal bonds relative to Treasuries but also suggest that municipal bonds are offering yields that are attractive under current market conditions.

The market also saw an uptick in trading activity, with senior fixed income portfolio manager Kim Olsan from NewSquare Capital indicating that municipals took advantage of favorable ratios across the yield curve. The most substantial increase in secondary market activity was noted outside the ten-year maturity range, where a pronounced slope of more than 50 basis points incentivized more aggressive bids. Nevertheless, Olsan cautioned that as we move further into December, specific longer-dated structures may encounter resistance levels.

In terms of new issue offerings, a recent sale of revenue bonds by Florida Turnpikes was particularly notable, as was the pricing by the California Municipal Finance Authority, both of which reflected notable interest from investors. However, the issuance landscape witnessed a slowdown in November, with the month ending with a total of $24.1 billion—marking a 34.6% decline from the previous year. Yet, robust demand persists, bolstered by anticipated redemptions of $37 billion due in December, which is expected to provide short-term leverage for the municipal market.

As December progresses, analysts believe there may be a continuation of the positive momentum for municipal bonds. The redemption trends and relatively strong demand, combined with the market’s ability to adapt to external pressures, suggest a favorable outlook. Historical data indicates that December usually yields moderate returns, and the performance in the preceding months may pave the way for continued investor confidence. If current trends hold, especially in the face of potential volatility from USTs, it’s reasonable to expect that municipal bonds could sustain their upward trajectory and remain attractive to both institutional and retail investors alike.

Leave a Reply