The landscape of municipal bonds, particularly Build America Bonds (BABs), has recently encountered significant turbulence. Factors such as fluctuating market conditions, escalating ratios, and rising interest rates have contributed to a noticeable slowdown in BAB redemptions. Despite the challenging environment, numerous issuers have expressed their intentions to call back their BABs before the end of the year. According to J.P. Morgan, approximately $14.9 billion of BABs have been called in 2024, with an additional $938.3 million planned for redemption. This trend underscores the ongoing demand for financial maneuvering among issuers in response to prevailing market conditions.

Year-to-date figures illustrate that 39 issuers have successfully priced deals aimed at refunding their outstanding BABs. Earlier estimates suggested that around $30 billion worth of BABs could potentially be redeemed through extraordinary redemption provisions (ERPs), a strategy that issuers began employing post a favorable court ruling deemed to allow such actions. However, the economic rationale behind these decisions strongly hinges on interest rate differentials. As highlighted by Nick Venditti, head of Municipal Fixed Income at Allspring, issuers are likely to proceed with refundings only when interest rates fall substantially below current levels.

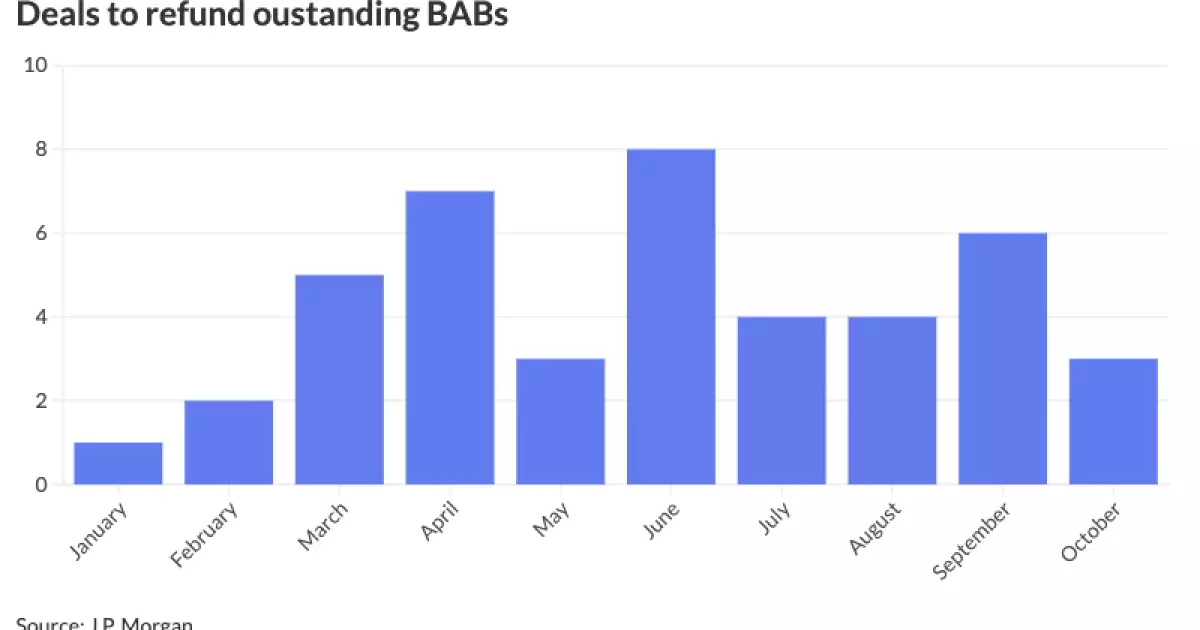

The trend in BAB refundings has not followed a consistent pattern throughout the year. J.P. Morgan’s data reveals a slow uptake in the first quarter, a peak in activity during the second quarter, and a noticeable decline in the third quarter of 2024. Notably, June was the standout month with eight transactions completing the market cycle, while January was relatively quiet with only one deal. The variances in market engagement underscore not only the economic climate but also seasonal influences affecting issuers’ urgency to refinance.

The Los Angeles Unified School District made headlines with a $2.9 billion general obligation (GO) refunding bond, marking the largest BAB refunding transaction in recent months. James Pruskowski, chief investment officer at 16Rock Asset Management, mentioned that the surge in activity seen in the second quarter sharply decreased, largely attributable to higher interest rates discouraging issuers from pursuing further refundings. Moreover, as municipal-UST ratios increase due to the underperformance of tax-exempt bonds over the past few months, the future likelihood of issuers leveraging ERPs to call back BABs appears diminished.

One critical incident illustrating the impact of market volatility involved the Ohio Water Development Authority’s decision to withdraw a $102.02 million bond offering intended for refunding Series 2010A-2 BABs. The authority projected negligible net present value (NPV) savings due to market fluctuations, prompting a strategic pause in their plans. Mike Fraizer, the executive director, clarified that they intend to revisit their BAB refunding strategy once market conditions stabilize, emphasizing their goal of securing more favorable financial outcomes.

Despite the controversies surrounding certain issuers, many remain committed to proceeding with their plans. For example, the Regents of the University of California recently called their outstanding BABs, illustrating the complexities in navigating refunding processes amidst legal uncertainties. However, firms like Ballard Spahr are continuing to actively participate in BAB refundings, as evidenced by their involvement in a $177 million refunding deal for Baltimore County. Teri Guarnaccia from the firm noted a lack of significant concerns from bondholders regarding recent transactions, implying a level of confidence within the market participants.

As the market continues to evolve, it is crucial for investors to reassess their perspectives on BABs, which have arguably become “super cheap” due to associated call risks. Venditti commented that the taxable municipal bonds are increasingly appealing to institutional investors seeking to better align their assets and liabilities. The potential impact of a call can yield adverse performance implications, deterring investor interest in BABs.

Sequestration has notably shaped issuer behavior, prompting many to call back their BABs as the full interest rate payment subsidy is no longer guaranteed. Venditti warns that the current dynamics render BABs almost “uninvestable,” particularly in the absence of robust legislative language to bolster investor security. Consequently, while some issuers are moving forward with refundings, a generalized wariness persists, necessitating a reevaluation of any forthcoming BAB or similar products in the market.

The interplay of market volatility, evolving interest rates, and strategic issuer decisions will continue to influence the realm of Build America Bonds. Investors and issuers alike must navigate this complex environment while being cognizant of the broader economic context shaping the future of municipal finance.

Leave a Reply