In the complex landscape of modern finance, market movements often tempt us to see patterns as either signs of growth or warning signals. However, beneath the surface of seemingly minor shifts in bond and equity markets, a more nuanced story emerges — one that challenges the optimistic narratives and demands a skeptical eye. Despite the apparent quietness in bond markets, with munis and U.S. Treasuries experiencing slight cheapening and equities posting gains, a deeper analysis suggests that these fluctuations may be less about resilience and more about underlying vulnerabilities.

The mild rise in yields, while superficially benign, could be indicative of simmering risks that aren’t immediately visible. The market’s momentum, described as “probably carried things a little too far,” hints at an overextended rally that’s ripe for correction. When markets extend beyond their natural bounds, it’s often an early warning that a period of adjustment or even decline could be imminent. This isn’t doom-mongering but a prudent reminder: complacency in the face of minor gains may overlook the building pressures of supply, inflation fears, and the natural ebb and flow of investor sentiment.

The Illusion of Robust Returns: A Closer Examination

Investment-grade munis are showing gains of roughly 2.7% month-to-date and over 3% for the year, numbers that might inspire confidence. But are they sustainable? High-yield munis are also reporting positive returns, yet these figures can obscure the underlying risks embedded in these assets. Taxable munis, with a 6.8% YTD return, appear attractive on paper, but with yields at or below 2%, the room for error remains slim. Such rich valuations are often unsustainable and susceptible to swift corrections if market sentiment shifts.

Furthermore, the trajectory of longer-term bonds, which have seen considerable outperformance, suggests a market that’s perhaps overpricing extension. Gains of over 4.5% in long-term indices over just a couple of weeks can be viewed as a reflection of aggressive positioning—something that might not hold in a less favorable environment. A natural market correction might bring these lofty gains back toward realistic levels, exposing vulnerabilities in the so-called “stellar” performance.

The perceived stability of curves, such as the AAA muni 30-year/10-year slopes, being more than double the comparable UST curve, exemplifies the disconnect between market perception and fundamental value. Does a steeper slope truly reflect market confidence, or is it a sign of risk mispricing? Many investors chase high yields, not necessarily because they see solid fundamentals, but because they’re seeking refuge in what appears to be safe despite potentially lurking risks.

The Danger in “Stable” Flows and Shifting Supply Dynamics

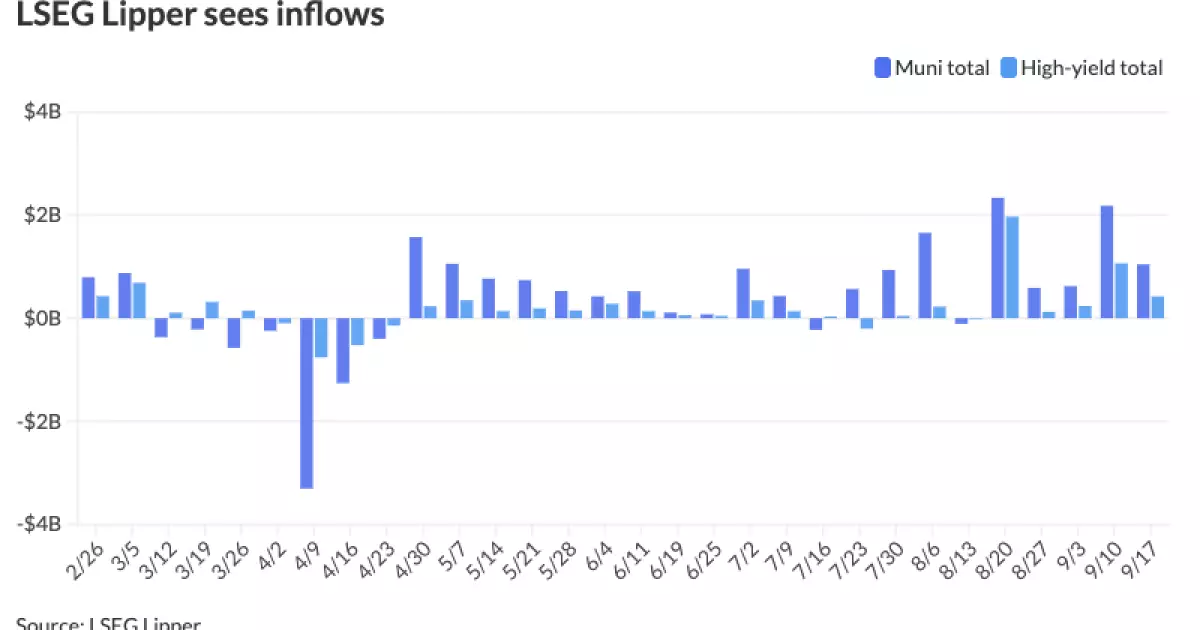

While inflows into municipal bond funds might appear positive, the reality is more ambiguous. Recent data reveals moderation rather than growth, with inflows slowing after a period of massive entries. Outflows from tax-exempt money market funds reflect a cautious stance — even amid generally positive market returns. This illustrates a crucial point: investor sentiment is hesitant, possibly wary of overvaluation or impending correction.

The modest increase in CUSIP requests for new municipal securities and the small yet persistent adjustments in yield curves signal a market that is delicately balanced. Elevated supply, expected to pick up in the fall, could exert additional pressure, especially if investor appetite diminishes. The risk is that what appears as stability today might swiftly morph into volatility tomorrow. The market’s tendency to “get overdone” underscores the importance of skepticism—what looks like resilience could be a facade hiding fragility.

The Hidden Risks in the “Safe” Bonds

Despite the seemingly attractive yields, the reality is that many bonds are trading at premiums, with valuations suggesting a bubble-like scenario. For instance, Georgia’s GO 5s at a mere 2.01%, despite a low ratio to the UST, exemplify the risk of overvaluation. Investors might be lured into these securities under the illusion of safety, but the underlying risks—be they economic, municipal, or credit-related—are not eliminated by yield alone.

Longer maturities, often seen as safe havens, are particularly vulnerable. Recent yield movements reveal that the market is adjusting dynamically, but not necessarily in a way that favors the investor. The market’s recent behavior underscores a subtle but persistent risk: investors are potentially overestimating the duration and safety of their holdings, which could lead to significant losses if fundamentals weaken.

Moreover, the widespread use of complex strategies such as short call structures in the short-term range signals a market seeking yield at possibly inflated prices. Given the rich valuations, these strategies may not provide enough cushion during downturns. The risk is a market that looks stable on the surface but is fraught with vulnerabilities that could trigger sharp corrections.

Market movements in 2024 may appear subdued and manageable, but a contrarian perspective reveals an underlying tension. The combination of high valuations, stretched yields, and cautious investor flows darken the optimism. The tendency to chase returns in a market that’s potentially overextended is a classic setup for a fall—one that savvy investors should heed before blindly succumbing to the allure of apparent stability. In this environment, skepticism is not just prudent; it is essential. The markets may be masking vulnerability, but the true test of resilience will come not from the calm of today, but from the storm that lurks just over the horizon.

Leave a Reply