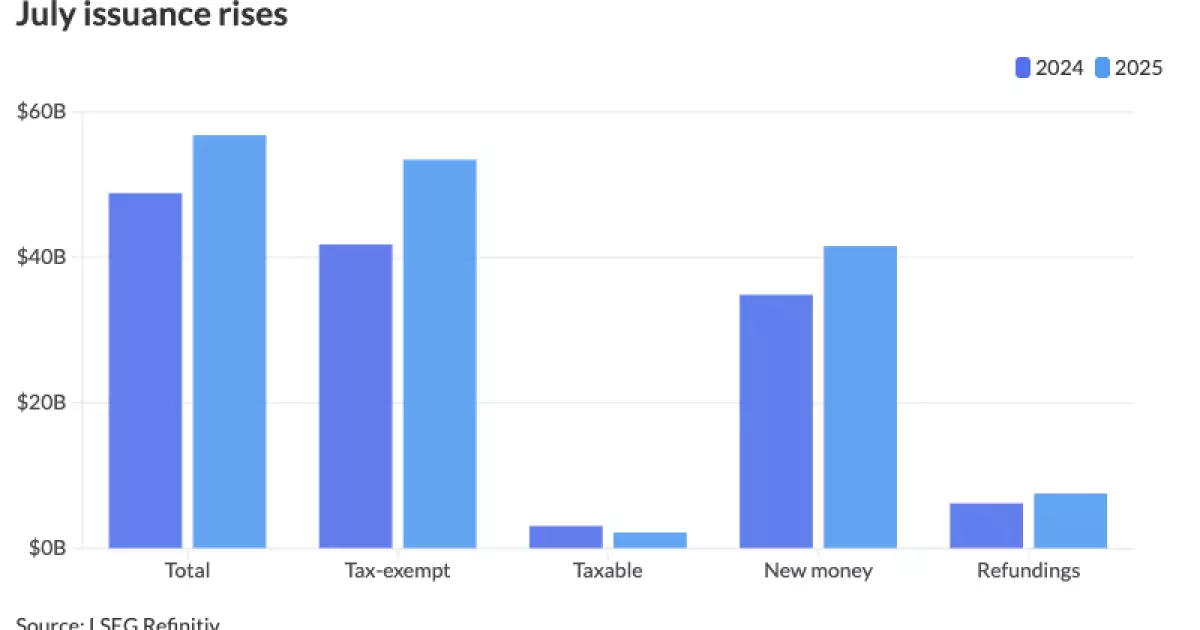

The municipal bond market has experienced an extraordinary surge in issuance during the first half of 2025, defying the usual cautious pace that historically characterizes the sector. While some might hail this as a sign of confidence in the economy, beneath the surface, this relentless push raises red flags about future stability and financial discipline. The aggressive volume—reaching over $280 billion — signals not just optimism but hints at a market driven by desperation and strategic frontloading. Governments and institutions, under pressure from political and fiscal uncertainties, are rushing to lock in capital before potential policy shifts or market downturns could threaten their financing avenues.

This frantic issuance raises questions about the true health of these borrowers. Are they genuinely capitalizing on favorable conditions, or merely hedging against future uncertainty? With the market environment characterized by high interest rates and volatility, such relentless borrowing might create a false sense of security, paving the way for future distress when market conditions shift unexpectedly. It is a textbook case of short-term thinking overriding long-term prudence—an attitude that could haunt the sector when the current tide recedes.

Market Volatility and the Illusion of Robustness

The environment that has fueled this unparalleled borrowing spree is paradoxical. While seemingly thriving with record issuance, the market has also been remarkably volatile, especially driven by tariff concerns, policy uncertainty, and shifting fiscal debates. This apparent contradiction underscores a flawed optimism—that market conditions always favor issuance. Yet, history suggests that such peaks are often followed by corrections, sometimes abrupt, exposing vulnerabilities that were obscured during the boom.

Current high interest rates, which ostensibly offer more income on new issues, serve as a double-edged sword. For issuers, they provide a cushion, but for investors, the prospects for sustained returns are less promising. Furthermore, the fact that issuers are rushing to market despite high volatility indicates a strategic anxiety—an urgency to finalize deals before conditions sour. The fear of missing out on favorable finance options becomes a dominant force, perhaps blinding market participants to long-term risks that could manifest once interest rates stabilize or decline.

This frenzied pace of issuance, especially with several weeks surpassing $20 billion, reflects a band-aid approach. It is a sign that issuers are betting heavily on short-term market momentum rather than strategic, sustainable planning. Such behavior dangerously assumes perpetual market optimism—which, history indicates, rarely persists indefinitely.

The Political and Fiscal Dimensions Fueling Excessive Borrowing

One of the most concerning drivers behind this surge is political uncertainty—specifically fears surrounding the potential loss of tax exemptions. The expectation that exemptions might be trimmed or eliminated has caused issuers to accelerate deals, frontloading volume to lock in benefits before policy changes occur. This is a shortsighted reaction characteristic of a sector that often reacts emotionally to political headlines rather than adopting disciplined, forward-looking financial strategies.

The recent bipartisan passage of a major tax and spending bill that spared key exemptions provides some relief; however, the broader pattern of tactical borrowing remains. Public universities, for example, have taken advantage of market conditions to fund substantial capital projects amid federal funding freezes and budget cuts. This behavior suggests a reactive sector that often prioritizes immediate liquidity over long-term fiscal health—particularly in high-profile sectors like education and infrastructure, which are vulnerable to political tides.

The implications for taxpayers and the broader economy are significant. Borrowing at such a scale to meet short-term needs or to capitalize on perceived opportunities can lead to structural deficits. The false sense of security generated by low-interest rates combined with aggressive issuance could embed long-term fiscal weaknesses, especially if the market experiences turbulence or policy shifts that reduce borrowing capacity or increase borrowing costs.

Forecasts, Realities, and the Risks of Overconfidence

Recent upward revisions of issuance forecasts—expected to top $600 billion—demonstrate widespread optimism but also highlight a dangerous overconfidence within the sector. Industry analysts are revising predictions upward, driven by the extraordinary issuance data already recorded, but these projections may be problematic if underlying market fundamentals deteriorate or if recession risks deepen.

While bond markets traditionally function as indicators of economic health, overissuance can distort this signal. When supply outstrips genuine demand—especially driven by issuer panic or strategic preemptive deals—the market could become overwhelmed. The current pattern suggests that market participants are becoming complacent, lulled into feeling that record volumes are sustainable, even desirable. This complacency is risky; if investor sentiment sours or macroeconomic conditions worsen, the sector could face sharp correction, with interest rates rising further and refinancing becoming more difficult.

Overall, this relentless issuance, while showcasing short-term confidence, suggests a disconnect between current market exuberance and the underlying economic reality. If history is any guide, such overheated markets often end poorly—leaving taxpayers and investors to shoulder the fallout. The sector’s current trajectory hints at a bubble driven less by fundamentals and more by political necessity, investor optimism, and a desire to accrue benefits before policy or market conditions inevitably change.

Leave a Reply