The municipal bond market’s recent behavior reveals a puzzling contradiction: despite attractive valuations and solid technical fundamentals, muni bonds remain in a low-volatility limbo without any meaningful breakout. Over the past several weeks, yields in short maturities have nudged slightly lower, but the longer end remains stubbornly unchanged. This lack of momentum suggests investors are cautious, even though yields on municipals are relatively cheap compared to Treasuries across most maturities. The essential problem here is that while demand appears strong, especially for deals with wide spreads, that demand is insufficiently robust to catalyze a sustained uptrend in prices or outperformance relative to Treasuries.

Why the Tepid Demand Despite Large Reinvestment Opportunities?

One would expect that the influx of substantial July reinvestment cash—estimated at over $47 billion in maturing and called principal and interest—would unleash a wave of buying and spark notable gains in muni prices. Instead, inflows to municipal mutual funds have been incremental, with last week’s $76.9 million inflow being the smallest in a sustained positive streak. The puzzlingly muted response hints at a deeper investor hesitancy. From a center-right liberal perspective, this hesitancy likely stems from skepticism about risk and reward in a post-pandemic world where government fiscal spending and borrowing have ballooned. Investors may be wary of the long-term viability of muni issuers despite the short-term security of principal repayments.

A Market Looking for a Catalyst—But None Is Coming

Despite multiple positive signals—modestly increasing yields, historically favorable after-tax spreads especially on higher-grade deals, and a steady, if restrained, primary market—the muni sector cannot seem to generate enthusiasm. The Birch Creek strategists’ candid admission that market participants “believe the market is cheap but are struggling to identify a catalyst” strikes at the heart of the issue. It rings true that for muni bonds to outperform, something beyond routine technical factors is required—an unexpected macroeconomic development, a significant fiscal stimulus to municipalities, or a sharp shift in investor sentiment. Without such a catalyst, the muni market risks drifting aimlessly, vulnerable to external shocks rather than proactive growth.

The Slow Burn of Credit Concerns and Political Realities

Beyond pure market technicals lies the murky reality of political dynamics affecting municipal credit quality. Many large issuers, particularly in high-redemption states such as California, New York, and Florida, are grappling with rising costs, pension liabilities, and uncertain tax revenues. While the market currently prices these credits as ‘investment grade,’ the underlying fiscal challenges are not trivial. From a center-right standpoint, the limited appetite in munis could reflect a cautious reassessment of government efficiency and financial discipline at the local and state levels. Investors may be discounting future political risks, such as tax hikes or spending cuts, which could threaten bond service payments down the road.

Primary Market: The Unsung Hero or a Temporary Fix?

In the face of modest secondary market activity, the primary issuance pipeline remains surprisingly active and well-received. Large deals from California’s Community Choice Financing Authority and New York’s State Thruway Authority demonstrate healthy institutional appetite for municipal debt, especially with projects tied to clean energy and transportation infrastructure. Still, the approach of a holiday-shortened week and relatively small issuance volume raise questions about sustainability. The primary market’s ability to “soak up liquidity” from reinvestments helping to prop up prices is positive, but it might mask underlying weaknesses rather than fix them. The heavy reliance on institutional buyers for new issues makes the muni market vulnerable to shifts in credit appetite or regulatory change.

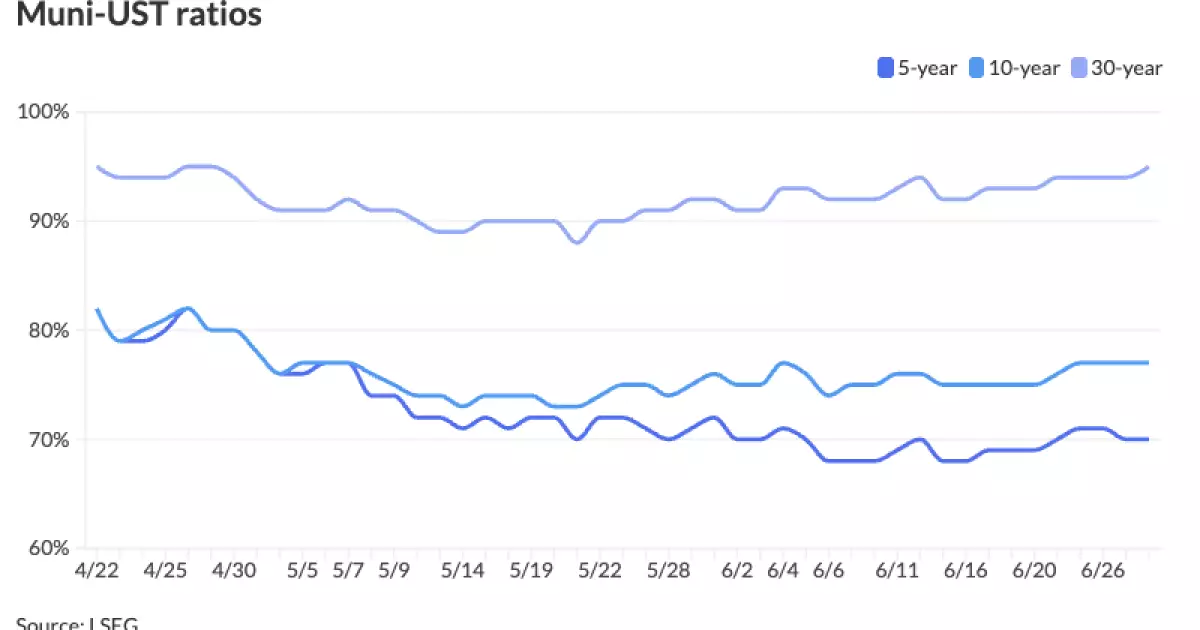

Valuation Paradox: Cheap Doesn’t Always Mean Attractive

The current stage for municipals, where yields are notably elevated on a tax-equivalent basis—some high-grade deals surpassing 8%—should theoretically lure yield-starved investors back aggressively. Logically, these yields should ignite a rally. Yet, the market remains subdued. This paradox suggests that valuation alone does not drive demand; investor psychology, macroeconomic uncertainty, and risk tolerance are equally crucial. The willingness to accept higher yields could signal investors are pricing in growing risks, or simply hedging for economic turbulence ahead. This asymmetry between yield attractiveness and cautious buying behavior highlights the complexity of the muni market’s current state.

A Tentative Outlook Colored by Cautious Optimism and Realism

Even as strategists forecast a “decidedly positive technical backdrop” driven by reinvestments and steady fund flows, the muni market faces an uphill battle for sustained investor confidence. The interplay of challenging political fiscal environments, lack of catalysts, and muted secondary-market liquidity breeds latent volatility risk. A center-right approach appreciates the soundness of fundamentals like principal protections and defined revenue streams but recognizes that government debt—no matter how local—cannot be immune to inefficiencies or policy uncertainties. Until these structural issues are transparently addressed or a new positive driver emerges, the muni market is likely to remain a cautiously approached investment, attractive in yield but tempered by risk aversion.

Leave a Reply