The municipal bond market has maintained a relatively stable posture in recent days, despite fluctuations in other financial sectors. On a recent Thursday, municipal bonds exhibited minor changes, even as they experienced a wave of inflows from mutual funds. Concurrently, U.S. Treasury yields showed an upward trend, ultimately leading to a dip in major equity markets. The current municipal-to-U.S. Treasury (UST) yield ratios highlight a mix of stability and opportunity for investors looking to navigate these waters. According to data from Municipal Market Data and ICE Data Services, the ratios indicate a balanced yet cautious market environment.

Two-year municipal bonds measured 62% of UST yields, while longer tenures reflected consistent, albeit varied, percentages—64% for five years, 67% for ten years, and 86% for thirty years. This proportional relationship signifies an ongoing interest in tax-exempt securities, even amidst a backdrop of rising Treasury yields. However, market experts highlight that the recent bullish momentum observed in UST yields does not parlay into the same enthusiasm for municipal bonds, particularly at the longer end of the maturity spectrum.

Tax-Exempt Trading Trends

While activity in the secondary market has been noted with a consistent demand for tax-exempt bonds, the longer maturities are missing the momentum necessary to produce robust performance enhancements. For instance, seasoned investment managers like Kim Olsan have tracked this trend, observing that the ten-year MMD yield currently hovers around the 2.75% mark—a notable deviation from the annual average. The thirty-year AAA rating must ascend by an additional 20 basis points to reach a 3.72% average.

Promisingly, flows toward longer maturities—those exceeding twelve years—have comprised a significant portion, with recent data reflecting over 55% of total tax-exempt volumes in this area. Various opportunities exist especially in high-quality names, where long-term maturities such as state general obligations (GOs) possess appealing coupons. These trends underscore a market shift towards capturing more favorable yield profiles, with investors opting for bonds structurally designed to offer greater returns.

In the primary market, a noteworthy development materialized with larger-sized bond offerings. Deals from entities such as the South Carolina Public Service Authority and the New York City Municipal Water Finance Authority have not only upsized but also demonstrated the demand for longer-term instruments. As yield curves flatten slightly, there is an evident increase in issuances, suggesting investor confidence complexes persist amid market fluctuations.

Furthermore, the broader implications of supply dynamics cannot be ignored. Negative supply projection—particularly in states like New York and New Jersey—has created a competitive landscape for in-state buyers. As firms reconcile the effects of upcoming redemptions, the situation presents a paradox where limited availability coexists with heightened demand, leading to tighter spreads for key issuances.

Gazing into the crystal ball, the upcoming March issuance and redemption cycle is poised to reshape the market landscape further. With New York currently bearing a projected negative balance nearing $2.21 billion, coupled with New Jersey’s similar projections, the pressure on the market could amplify. The interplay of negative supply combined with substantial in-state exemption values will merit close observance, especially when factoring in how these dynamics will influence spreads for AAA-rated bonds.

Market analysts caution that credit spreads will respond variably to these evolving conditions, with states such as Texas potentially facing a shortfall against redemptions. Conversely, Pennsylvania’s estimated positive supply of $451 million might lead to broader spreads, reflecting an intriguing divergence in state-level dynamics that merits close examination.

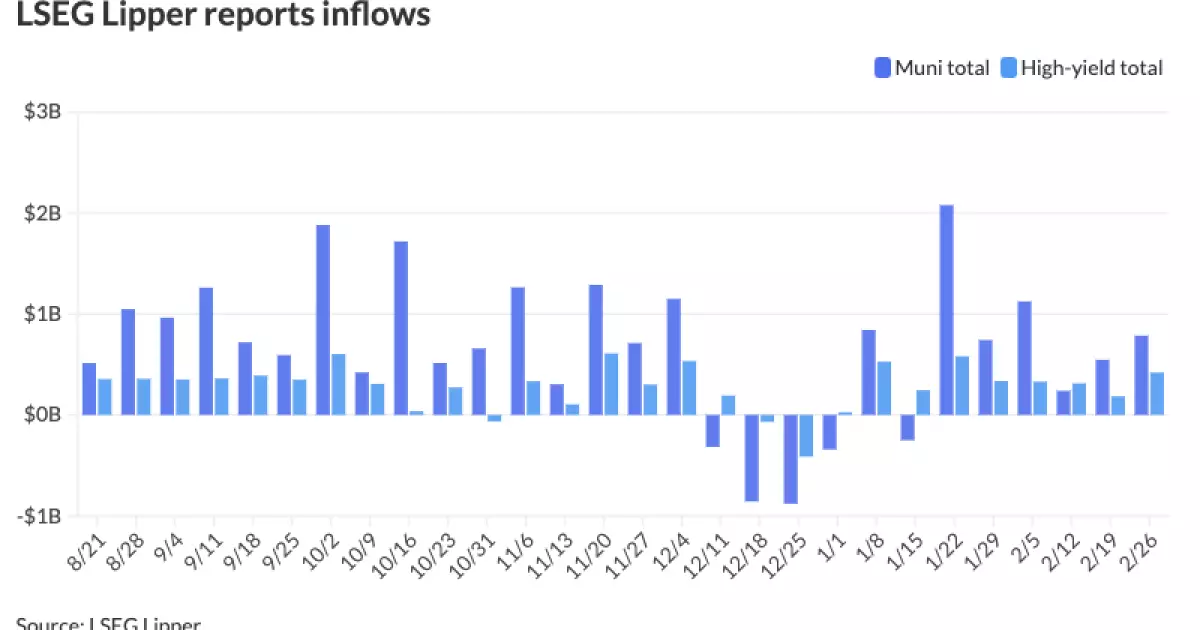

In conjunction with these observations, the flow of funds remains a critical element driving market sentiment. Recent reports illustrate that municipal bond mutual funds experienced an impressive inflow of $785.5 million, mirroring the healthy engagement of investors seeking tax-exempt avenues. High-yield funds, too, exhibited robust inflows, suggesting confidence in riskier municipal positions. Despite a pullback in taxable money-fund assets, indicators point towards a balanced tenacity among tax-free assets, with yields inching upward.

Moreover, as the SIFMA Swap Index reveals shifts in short-term yield patterns, municipal bond investment strategies may need re-evaluation. Investors should consider how these yield behaviors align with risk profiles while also trapping capital in competitive, albeit volatile, conditions that the municipal market tends to attract.

Navigating the municipal bond landscape during this period calls for a sharp focus on yield ratios, supply dynamics, and investor behavior. As municipal bonds stabilize amidst changing Treasury yields, the market signifies a blend of caution and opportunity. This delicate balance requires stakeholders to remain astute, adapting to shifts while positioning themselves strategically for potential unlocks in yield and asset appreciation. The interplay of supply, demand, and investor sentiment will ultimately delineate the trajectory of municipal bonds in the months ahead.

Leave a Reply