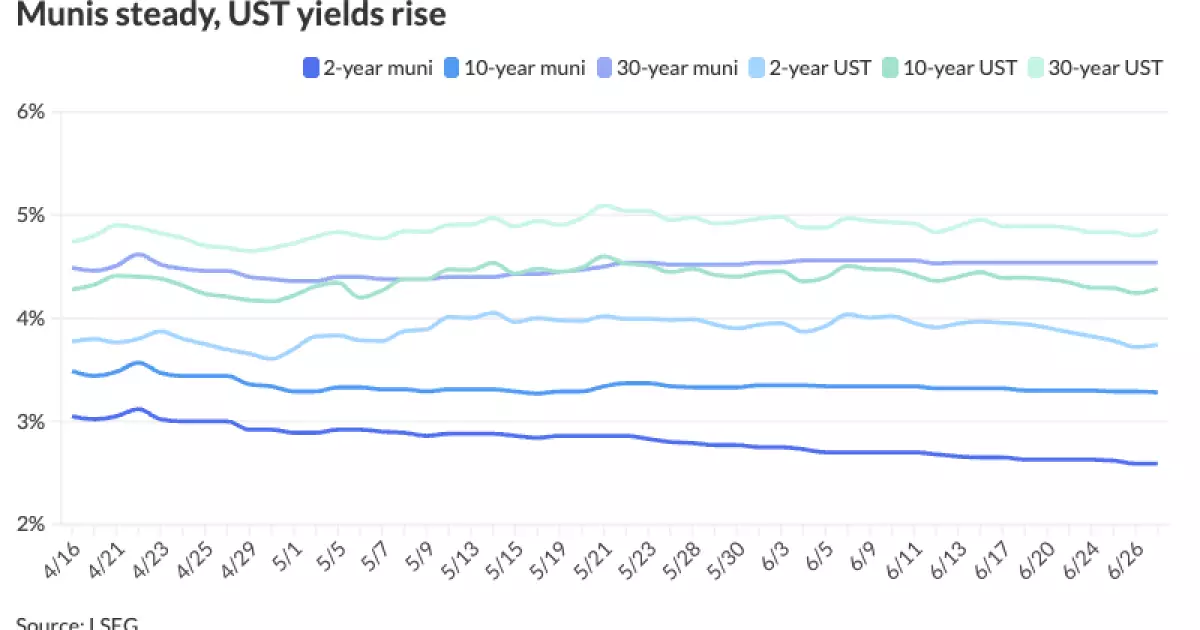

At a glance, the municipal bond (muni) market appears steady as we enter the mid-year point, with yields nudging upward and equities, notably the S&P 500 and Nasdaq, hitting record highs. But this surface calm conceals significant pressures beneath—a rising tide of issuance that threatens to overwhelm demand and strain valuations. While traders and strategists bask in the apparent resilience of tax-exempt muni securities, a critical eye reveals a looming imbalance driven by record municipal borrowing and its unpredictable ramifications.

Record Issuance is a Double-Edged Sword

June’s issuance shattered previous records with over $50 billion in new munis, a volume that has forced prestigious firms like Bank of America Securities (BofA) to revise annual issuance projections sharply upward—from $520 billion to an eye-watering $580 billion. This record pace hasn’t just surprised analysts; it has also reshaped market dynamics. Increased supply puts downward pressure on muni prices, causing them to underperform notable government securities such as Treasuries. Barclays strategists observed this trend clearly, noting that muni-to-Treasury ratios have risen, reflecting tax-exempt bonds selling off amidst heavier supply.

The problem is structural and ongoing. While BofA expects a balance between issuance and principal redemptions plus coupon payments in the second half of the year, Barclays anticipates a 10% drop in issuance relative to the first half. But even a slight dip may be insufficient to normalize a market flooded with new debt. The fundamental mismatch between ever-increasing issuance and inconsistent demand is a thorny issue that neither strategists nor investors seem eager to fully confront.

Muni Market’s Back-Loaded Returns and Investor Complacency

Munis have remained the sole fixed income asset class with negative total returns year-to-date—a striking fact that deserves more attention than it’s getting in investor circles. Barclays, maintaining a cautiously optimistic stance, suggests that performance is “likely to be back-loaded,” encouraging longer-duration positions heading into the second half of 2025. This outlook, though hopeful, veers dangerously close to wishful thinking.

For an asset class heavily tied to public sector health, muni market investors seem to be relying on a technical rebound fueled by maturity schedules and curbed new supply, rather than fundamental improvements. The risk? Investors are caught in a precarious waiting game, hoping seasonal patterns redeem their losses while ignoring the underlying stressors caused by ballooning debt levels and potential credit risks across municipalities—many of which face budgetary pressures unseen during the more flush pre-pandemic years.

Seasonality and Technicals: Are They Enough?

Historical data suggests the muni market often strengthens in July and August, with ratios typically declining and selling off modestly in August. This seasonal behavior, while helpful, is hardly a cure-all. The balance sheet of municipal borrowers is not reset by calendar months. The July-August window is likely to see “strong supply/demand mechanics” according to BofA, driven by higher redemptions and coupon payments offsetting fresh issuance. Yet, this equilibrium may only be temporary, as technical conditions are expected to deteriorate heading into the fall, when issuance outpaces redemptions.

Viewing these patterns as reliable predictors of muni market health is overly simplistic. The coordinated timing of massive new borrowing against maturing debt and coupon payouts screams complexity and vulnerability, not the calm before a predictable summer rally. Investors ignoring these nuances may be exposing themselves to nasty surprises in the second half.

Relative Valuation: A Mirage of Value

Proponents of munis highlight their historically attractive relative valuations compared to Treasury bonds, especially given the tax advantages that munis confer. However, beneath the favorable price tags lies a more unsettling truth: the negative total returns year-to-date expose fundamental weaknesses. That munis have slipped despite broader market gains suggests structural flaws, not mere valuation inefficiencies.

The current discounts may be better viewed as a “distress premium” rather than true value. When municipal entities face rising costs, pension liabilities, and fiscal constraints, the chances of bond underperformance rise. This makes the seemingly cheap muni market more a reflection of risk than bargain hunting. Investors seeking yield must demand caution here—tax exemption alone does not immunize bonds from credit stress or price volatility.

Increased Yields or Hidden Landmines? A Cautionary Take

Yields on municipal bonds, especially longer maturities, have climbed moderately, signaling both higher borrowing costs for municipalities and greater return potential for investors. Yet, these increases aren’t pure gifts. They represent the perceived increased risk baked into new issuance and continuing economic uncertainty for local governments.

For instance, Massachusetts Bay Transportation Authority’s massive bond sale highlights the reliance on senior sales tax receipts—an unstable revenue base in a shifting economic landscape. Similarly, high-profile taxable bond offerings in education and housing sectors emphasize the growing financial stress on public institutions forcing them to turn to taxable debt markets, which historically carries more risk and fewer incentives for investors.

The yield upticks, therefore, are not just healthier compensation but warnings—a call for investors to scrutinize credit quality and structural balance sheets carefully. This is not a market for passive trust but active due diligence.

Policy and Fiscal Discipline: The Missing Ingredient

From a center-right perspective, the challenges in the municipal bond space underscore a deeper malaise: chronic fiscal laxity and inadequate accountability at local government levels. Record borrowing reflects not only infrastructure needs but also long-standing deficits masked by kicking the can down the road. Without stringent reforms, we are unlikely to see sustained improvement.

This environment demands that investors insist on more transparency and enforcement of fiscal discipline. Public entities must embrace realistic budgeting, cut non-essential expenditures, and prioritize solvency to restore trust. Meanwhile, tax-exempt status should not be viewed as an entitlement but as a privilege contingent on solid financial governance.

Municipal bonds can remain a stable, tax-advantaged investment—but only if the issuing bodies take hard responsibility for their balance sheets. Otherwise, the muni market’s precarious gains risk unraveling, leaving taxpayers and investors to shoulder the fallout.

Leave a Reply